The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

The Scottish third sector tracker Waves 1-10 (Spring 2025)

The Scottish third sector tracker - waves 1-10 (Spring 2025)

Introduction

This paper considers some of the key longitudinal metrics from the first two phases (ten waves in total) of the Scottish third sector tracker. (Summer 2021 - Spring 2025)

Service and programme delivery:

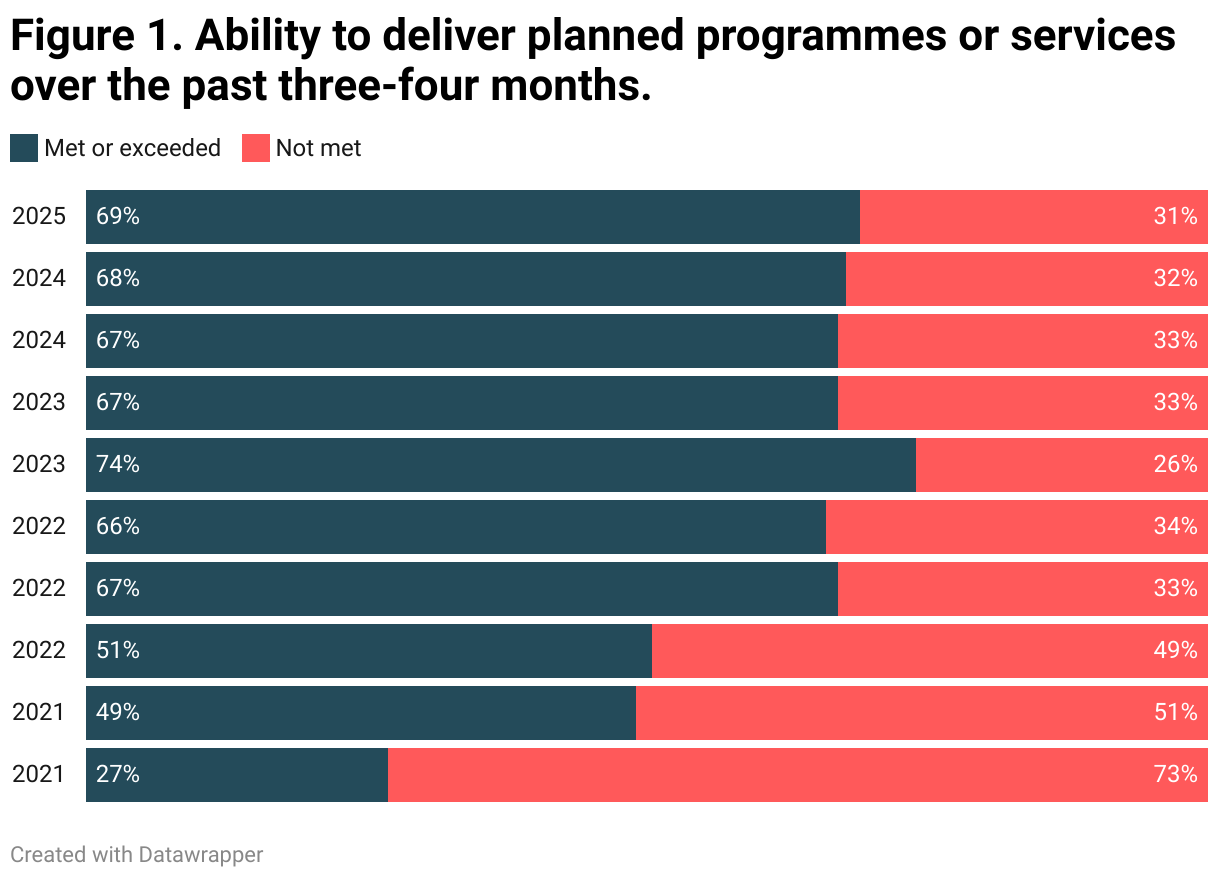

- Two-thirds to three-quarters of organisations have consistently reported being able to meet or exceed their planned work (excluding the early pandemic waves).

- Roughly one-third have been unable to deliver as planned in each wave.

Meeting demand:

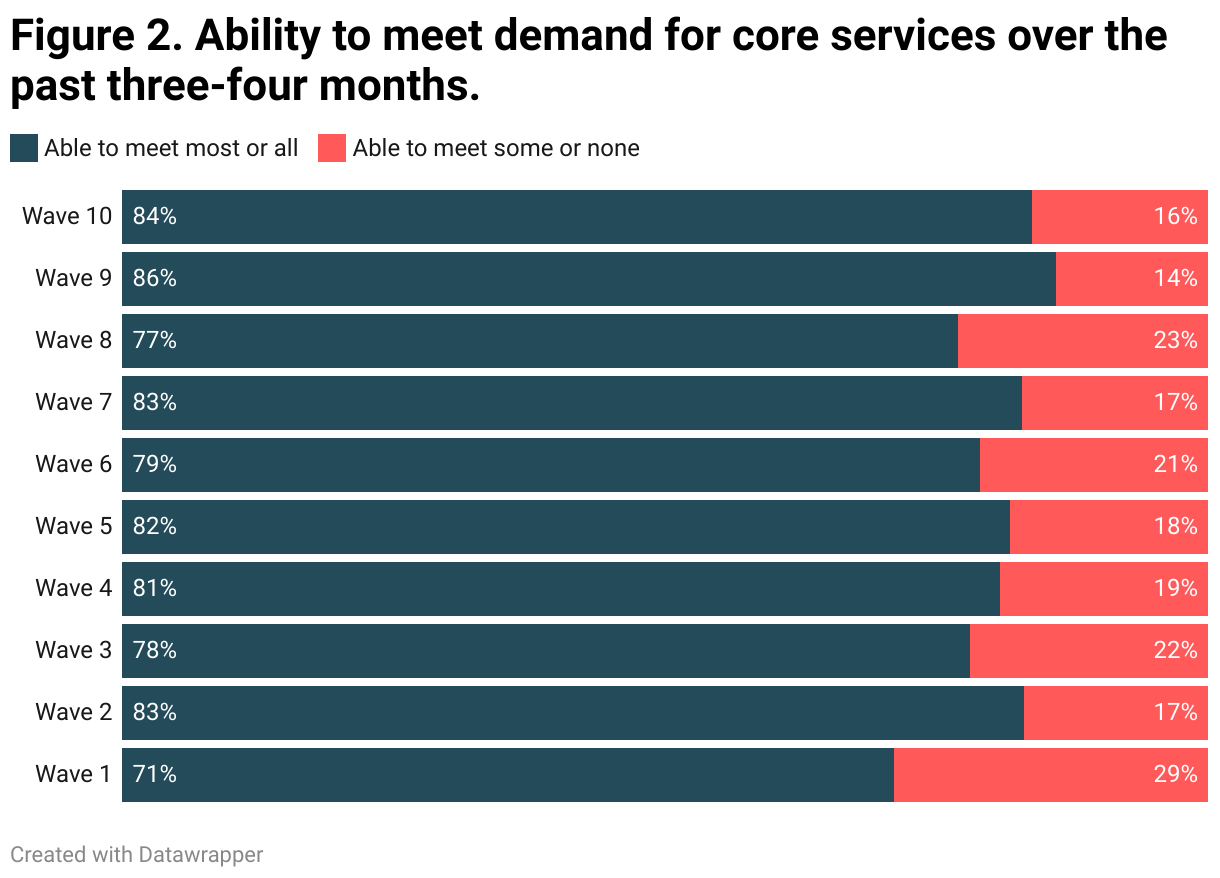

- The ability to meet demand for core services fluctuates but remains a persistent challenge for around one in five organisations.

Challenges:

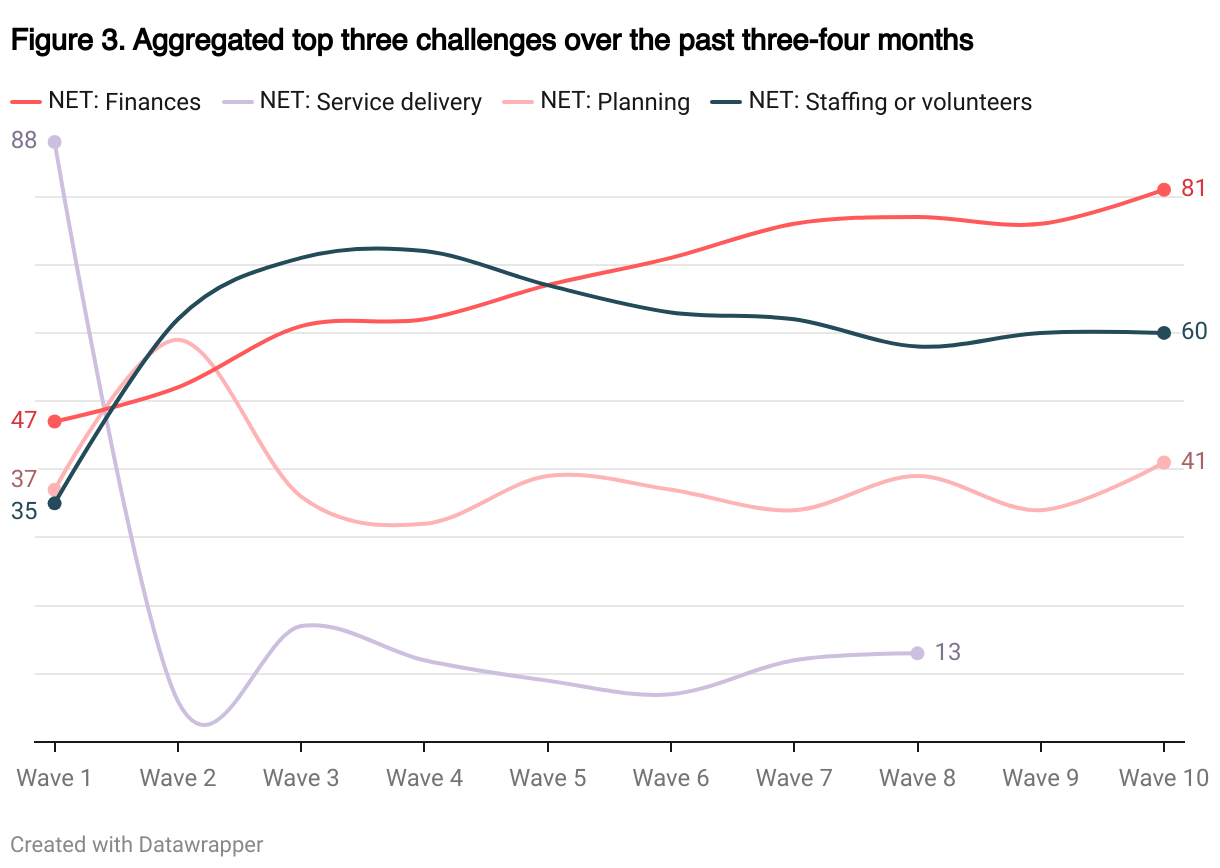

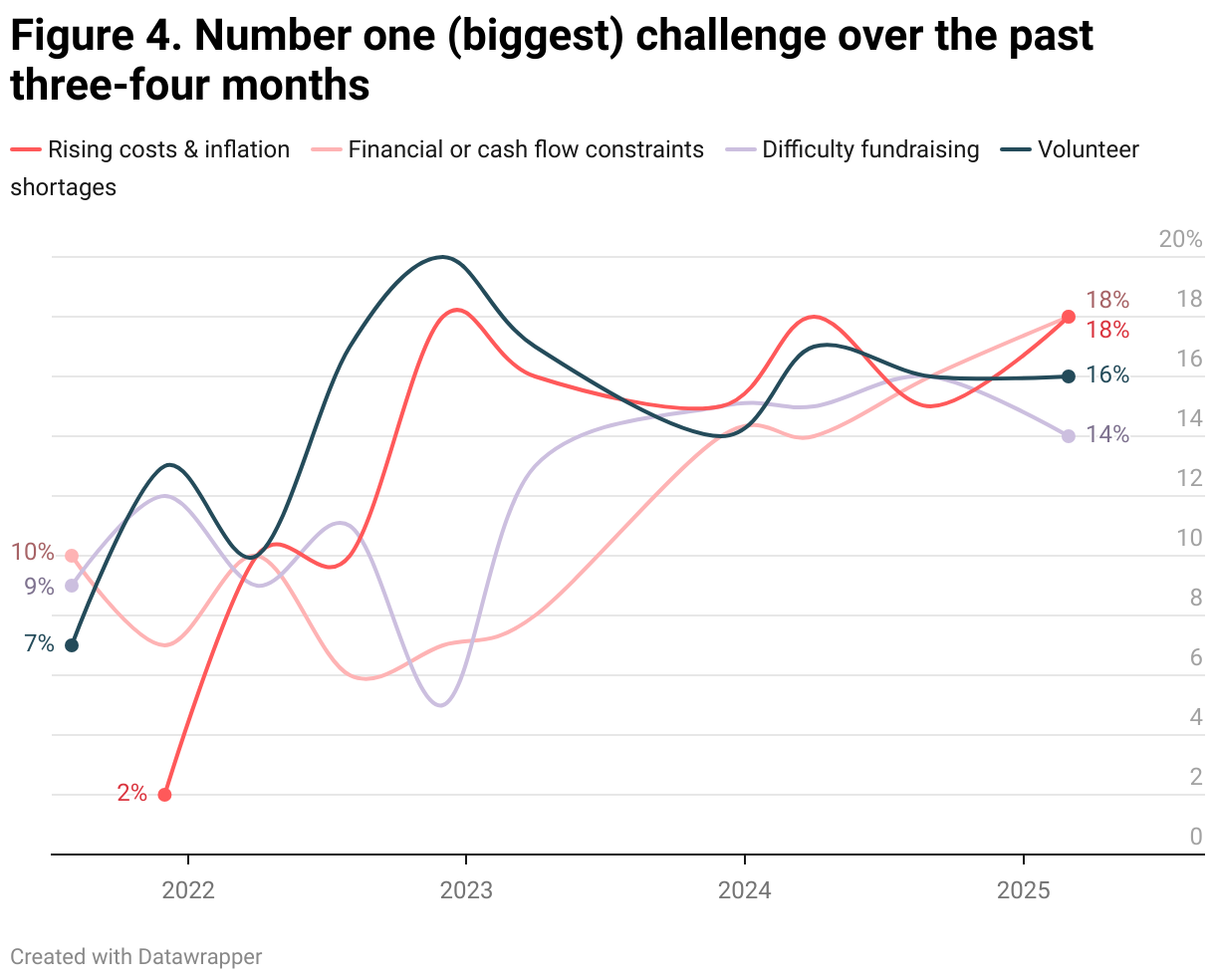

- Since April 2023 (wave 6), financial challenges have dominated the top three challenges.

- The biggest challenge has varied: Volunteer shortages was the top issue from December 2021 to December 2023. Fundraising difficulties, rising costs, and inflation are the primary concern in March 2025.

- Rising costs and inflation have been the leading issue since August 2022 and continue to grow in importance.

- Uncertainty about the future and cash flow constraints have also reached record levels.

Responding to challenges:

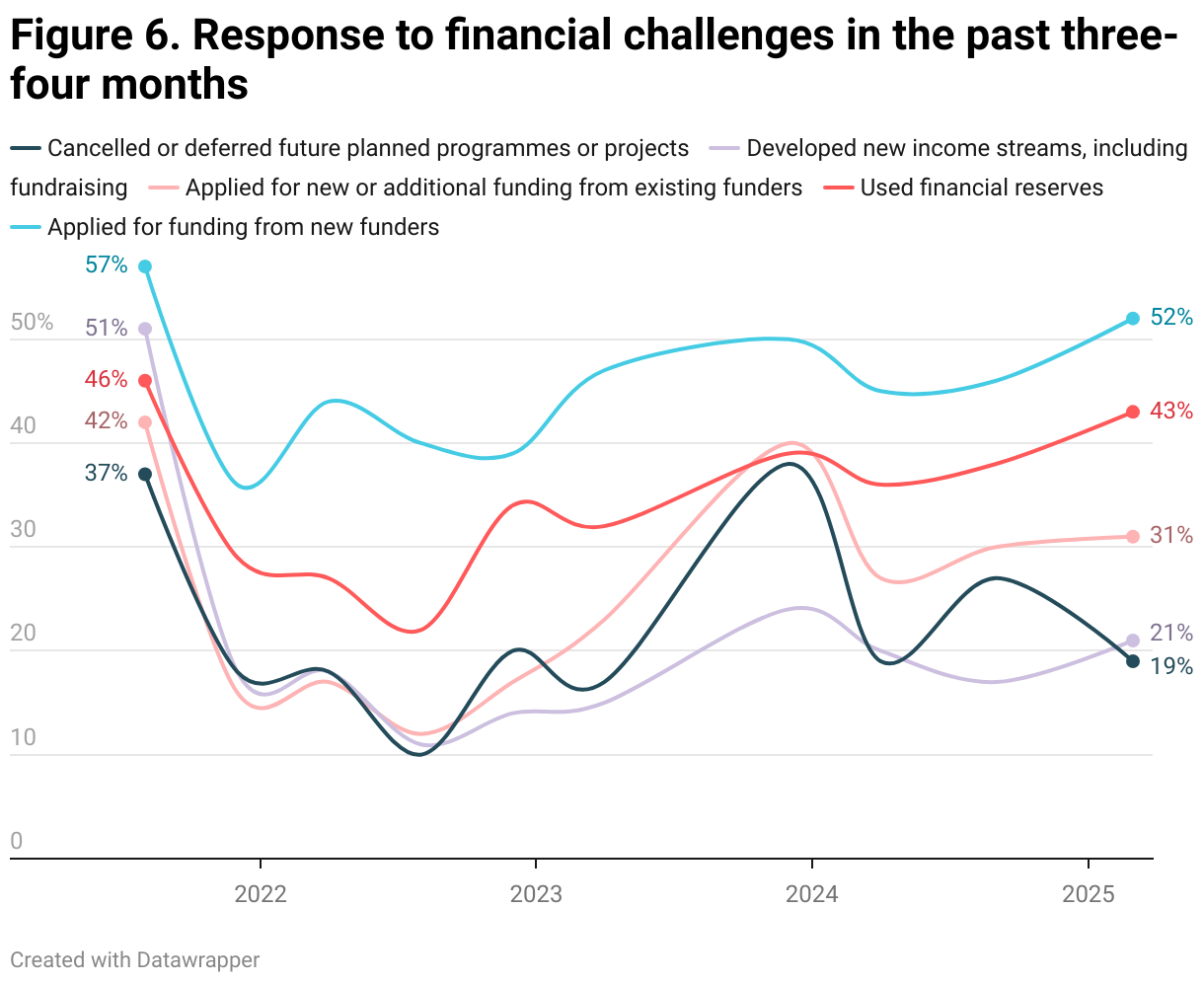

To manage financial pressures, organisations have most commonly:

- Applied for funding from new funders (52%)

- Used financial reserves (43%)

- Both actions are at their highest levels since the pandemic.

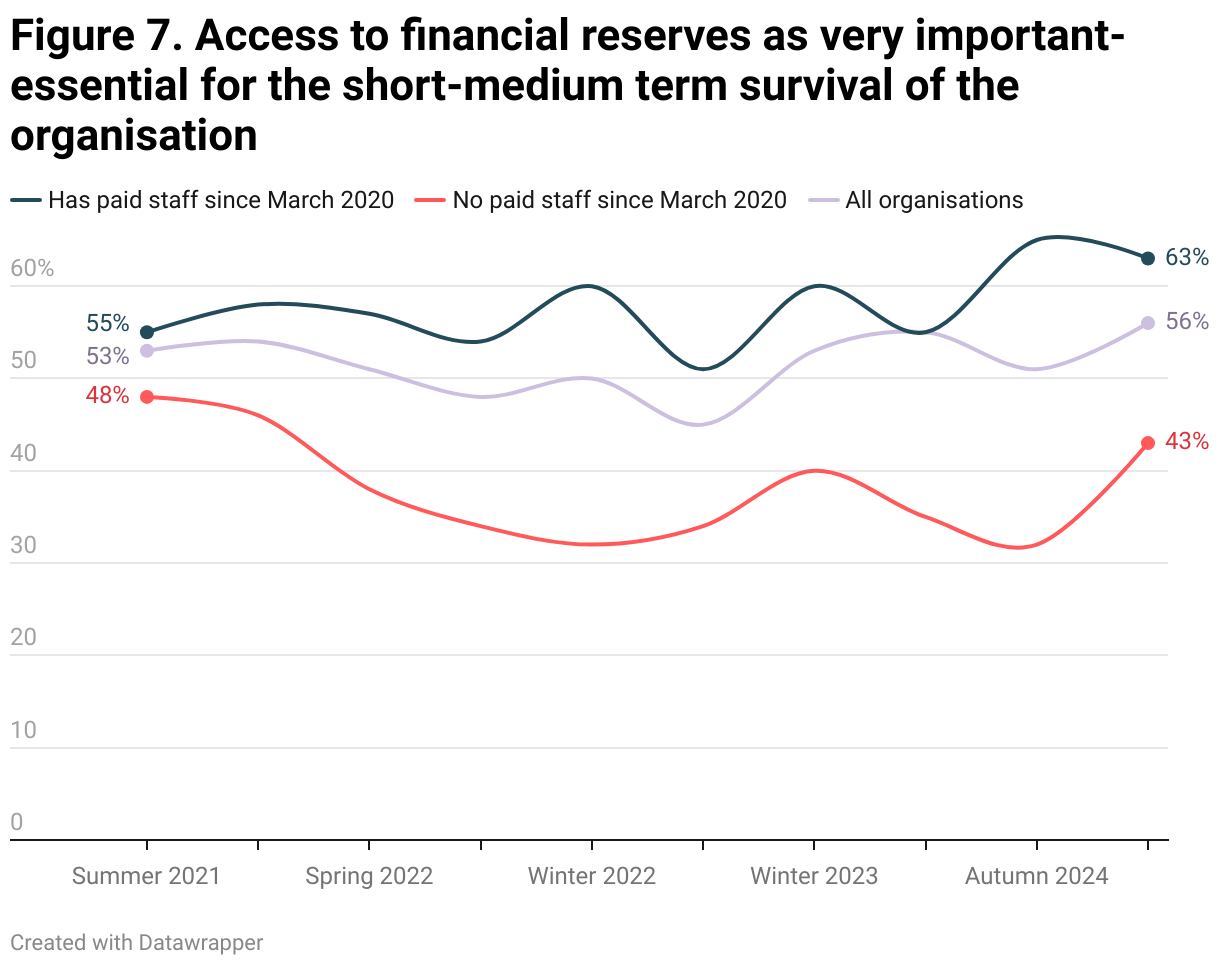

Financial health:

- A record 56% of organisations now say access to financial reserves is essential to their short- to medium-term survival.

- For organisations with employees, this figure rises to 63%.

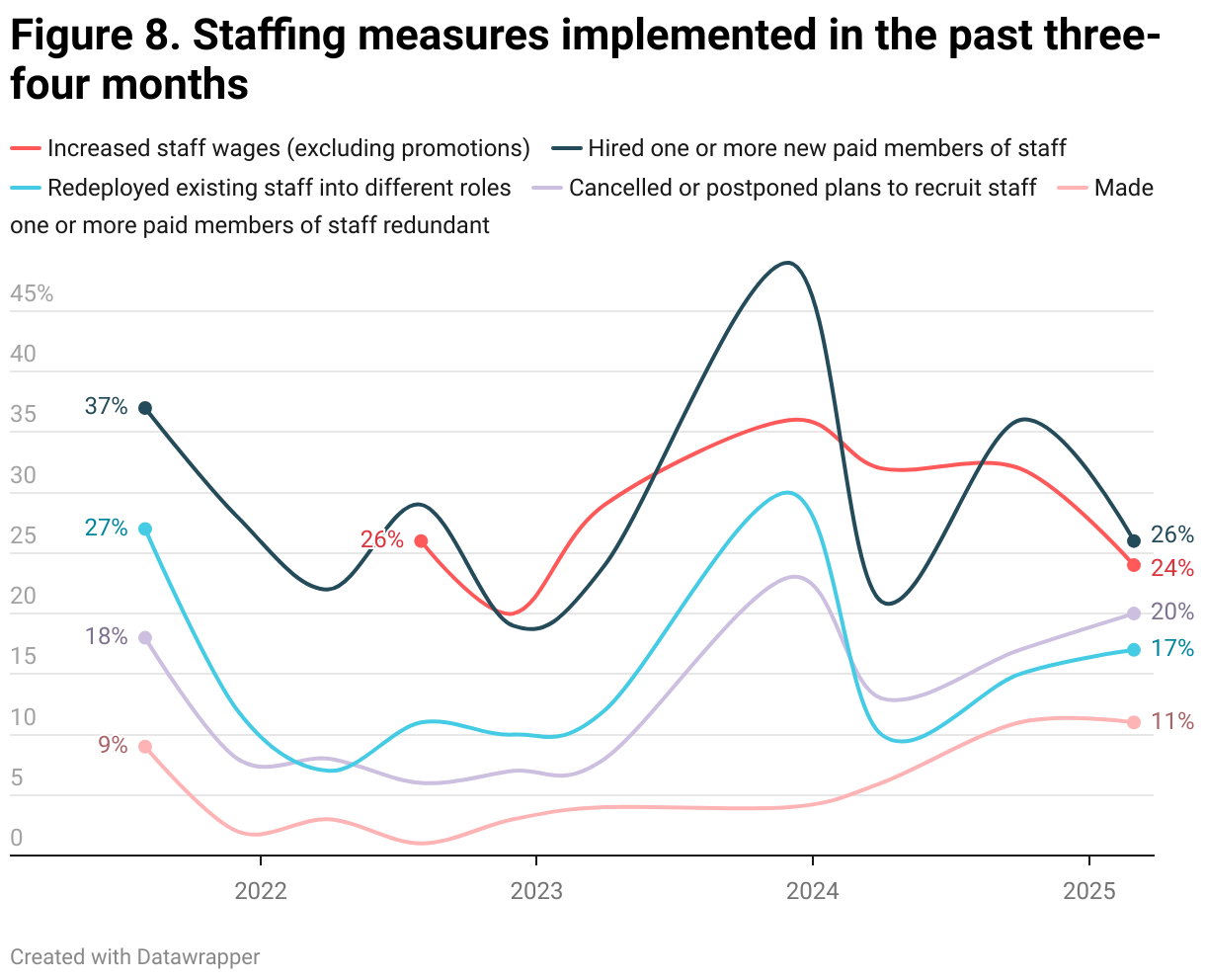

Staffing:

On average:

- One-third are hiring new staff.

- A similar portion are increasing wages, though this has declined since December 2023.

- 13% are cancelling or postponing recruitment, with this trend increasing.

- Redundancies are rising from an average of 5% to 11% currently.

This report presents key trends from waves one to ten of the Scottish third sector tracker, highlighting how organisations have managed service delivery, financial pressures, and staffing challenges in recent years. Despite early pandemic disruptions, two-thirds to three-quarters of organisations have consistently met or exceeded their planned service delivery, though about one-third continue to fall short in each wave. Meeting demand for core services remains difficult for roughly one in five organisations. Financial challenges have dominated since April 2023, with rising costs, inflation, and uncertainty about the future reaching record highs. In response, many organisations have turned to new funders (52%) and used their financial reserves (43%), which are now considered essential to survival by over half (56%) of all organisations. Staffing trends reveal careful hiring, increasing wage pressures, growing recruitment postponements (13%), and a doubling in the number of organisations making redundancies from 5% to 11%. The findings underscore persistent strain across the sector.

Organisations are asked to tell us if they have been able to deliver on their planned programme of work or to deliver their services over the previous three-four months. Apart from the first three waves (consequences of the pandemic), between two thirds and three quarters of organisations reported meeting or exceeding their planned work over the preceding three-four months. Approximately one third of organisations are unable to deliver as planned each wave.

Most organisations report being able to meet most or all the demand for their core services over the past three-four months. On average, one in five organisations struggle to meet all the demand for their core services at any given time.

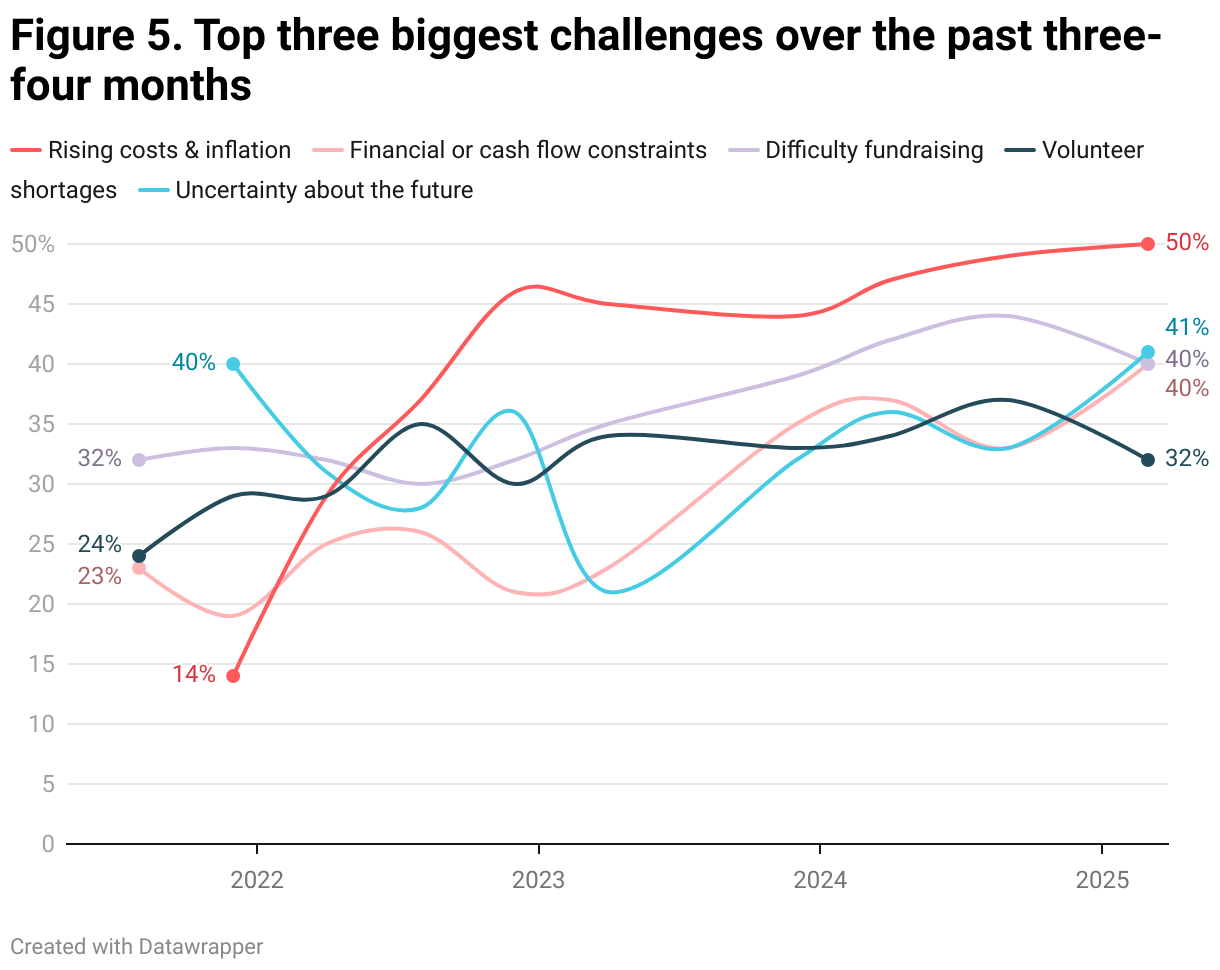

Respondents are asked to rank their top three biggest challenges over the past three-four months from 1-3. Aggregated, financial challenges have dominated the top 3 list since April 2023 (wave 6) onwards.

The challenge most frequently selected by respondents as their biggest challenge has fluctuated wave by wave. Volunteer shortages had a spell at number 1 from December 2021-December 2023 when it was usurped by difficulty fundraising and rising costs and inflation. Financial and cash flow constraints and rising costs and inflation are tied at number 1 in March 2025.

Disaggregating the top 3 challenges, rising costs and inflation has been a clear leader since August 2022 and has extended that lead. Uncertainty about the future and financial and cash flow constraints are at their highest levels on record.

In response to mounting financial pressures, organisations have acted. The two most frequent actions have been to apply for funding from a new funder (i.e. a funder that they don’t already receive funding from) and to use their financial reserves – both of those are at post-pandemic highs with half the sector applying for funding from a new funder (52%) and 43% using their financial reserves.

The number of organisations reporting that access to their financial reserves is very important- essential for their short-medium term survival is at record levels – 56% of the sector, this is more pronounced for those organisations that employ staff – 63%.

On average, across the ten waves of data around one in three organisations are hiring new staff at any given time. This is also true for organisations increasing staff wages, although the latter has been in a downward trend since December 2023. 13% of organisations are cancelling or postponing plans to recruit at any given time, with that trend generally increasing over time. Similarly, there’s been an uptick in the number of organisations making staff redundant – 5% of organisations on average across the ten waves but now sitting at 11%.