The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

The Scottish third sector tracker Wave 10 (Spring 2025)

The Scottish third sector tracker - wave 10 (Spring 2025)

Introduction

This paper presents the key findings from the ten wave of the Scottish third sector tracker, data for which was collected in February-March 2025. The Tracker collects panel data from Scottish third sector organisations to give current insights into the health of the sector, key trends, and developments. The Tracker asks organisations questions relating to their current organisational challenges; demand for their services; paid staff and volunteers; and financial health. Topical questions are included each wave. For wave ten, we asked respondents to tell us about the impact of increased National Insurance contributions and running a budget deficit.

The wave ten findings draw on responses from 326 third sector organisations. Surveys were conducted online. Quotas and weighting have been used to ensure the final dataset represents the Scottish third sector in terms of the organisations’ location, activity, and turnover.

The dataset contains a mix of quantitative and qualitative responses. Quantitative data were used to generate a series of summary figures and tables that present key insights into the sector over the last four months. A thematic analysis was conducted on qualitative responses to open questions. In each case, the most frequently reported themes have been highlighted. Supporting quotes for these and other noteworthy themes have been provided.

All the data for this report have been taken from the Scottish Third Sector Tracker.

Challenges:

- 93% of organisations reported facing challenges since Autumn 2024.

- Top-ranked issues included rising costs and inflation and financial and cash flow restraints (both 18%), followed by volunteer shortages (16%).

- Financial pressures have increased:

- 81% of organisations reported financial-related challenges, an increase of 10% since spring 2023.

- 58% applied for new funding, 43% used financial reserves, and 19% cancelled or deferred planned work.

- 37% of organisations reported operating with a budget deficit.

- Impact of rising costs:

- 60% said rising costs had a moderate or significant impact on service delivery.

- 11% stopped delivering one or more strands of work.

- Service delivery:

- 83% said they could meet most or all service demand, and 70% met or exceeded planned programmes—consistent with previous wave.

- Staffing challenges persist:

- 20% cancelled or postponed staff recruitment; 11% made redundancies.

- 41% found staff recruitment moderately to significantly challenging.

- Volunteer recruitment and retention issues:

- 55% reported difficulty recruiting volunteers; 40% cited retention challenges.

- Main barriers: fewer people coming forward, lack of time, and volunteer burnout.

- Concerns over Employer National Insurance increases:

- 70% expected a negative financial impact from increased employer ENICs.

- 41% anticipate effects on service or programme delivery.

- Reserves being heavily relied upon:

- 54% said their current use of reserves is unsustainable (↑14% since Autumn 2024).

- 56% consider reserves essential to their short-to-medium-term survival.

- Funding uncertainty:

- Only 13% had all 2025–26 funding confirmed at the time of survey.

- 36% had none confirmed; 45% had partial confirmation.

- Outlook and Support Needs:

- 89% of organisations are confident they will still be operating in 12 months.

- Top support needs: finding funding (49%), recruiting volunteers (31%), and IT/digital support (24%).

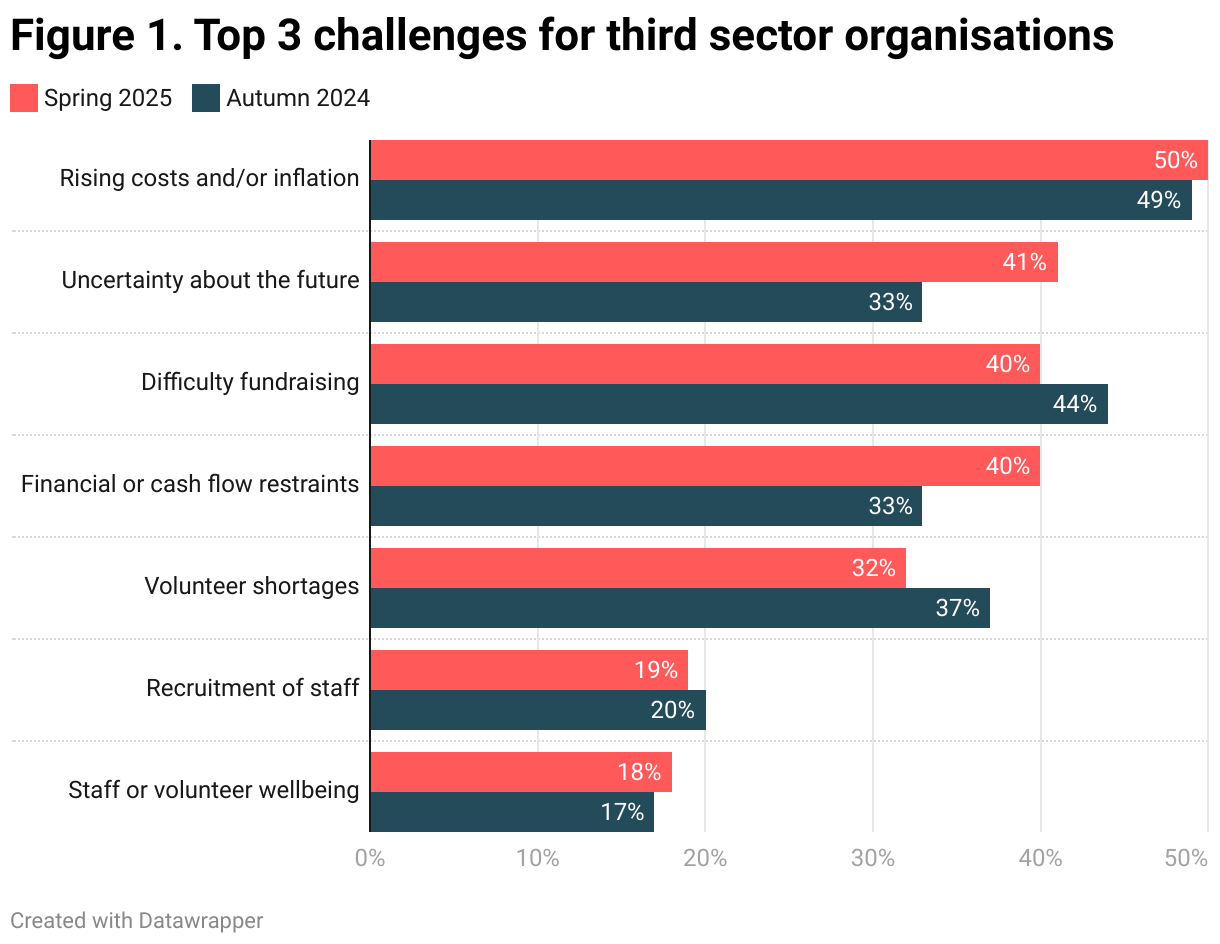

Organisations were asked about the biggest challenges they had faced since Autumn 2024. Ninety-three percent (93%) of organisations reported facing challenges, in line with Autumn. The response most frequently ranked as the number one challenge was a tie between Rising costs and inflation and Financial and cash flow restraints (both 18%), followed by Volunteer shortages (16%).

When considering organisations’ top three challenges, the most frequently reported were: Rising costs and inflation (50%); Uncertainty about the future (41%); Financial and cash flow restraints (40%) and Difficulty fundraising (40%). Uncertainty about the future and financial and cash flow restraints have seen the largest increases since Autumn, by 8% and 7% respectively.

Challenges relating to finances (81%) remain the most frequent response options selected by organisations.

Sixty percent (60%) of all organisations reported that rising costs had either significantly (19%) or moderately (41%) affected their ability to deliver their core services or activities since Autumn 2024. Only 13% of organisations reported no impact at all – these figures are in line with wave 9.

In the past four months, eight in ten organisations reported acting in response to financial challenges. The most frequently reported actions included, applying for funding (58%); using their financial reserves (43% ↑5%); and fundraising (21% ↓6%). Concerningly, 19% (↑2%) of organisations reported cancelling or deferring planned work and 11% stopped operating one or more strands of work.

Eighty-three percent (83%) of respondents thought their organisation had the capacity to meet most or all the demand for their core services across the last four months, again in line with Autumn 2024. Similarly, seven out of every ten organisations reported meeting or exceeding their planned programmes of work for the preceding quarter, also in line with Autumn 2024.

Organisations are asked about the key actions taken in relation to paid staff over the last four months. Of the organisations that employed paid staff, a quarter (26%) had hired one or more new members of staff, and a quarter (24%) had also increased staff salaries. However, one in five (20%) had cancelled or postponed plans to recruit staff. As per Figure 2, fewer organisations reported hiring new staff; increasing salaries; or promoting staff than in the four months leading to Autumn 2024. More organisations do report cancelling plans to recruit and redeploying staff into different roles. The redundancy rate remains unchanged, with 11% of organisations making one or more members of staff redundant in the last four months.

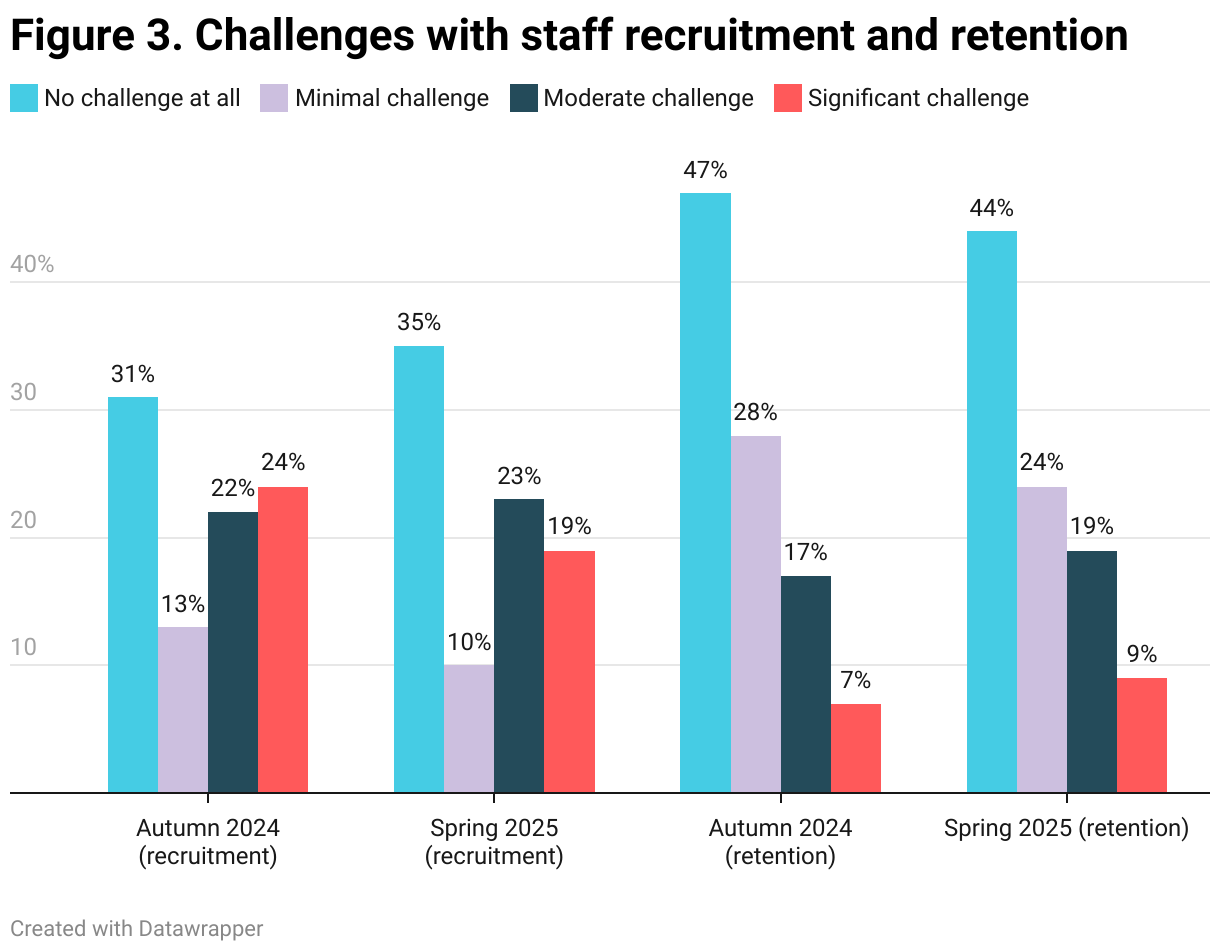

Staff recruitment and retention

We then asked organisations with paid staff if they had found recruitment or retention a challenge. Overall, organisations have found it more difficult to recruit staff than retain staff. Four in ten organisations (41%), reported a moderate-significant challenge in recruiting staff in the past quarter, down slightly from 46% in Autumn 2024. In Spring 2025, just over a quarter (27%) of organisations reported a moderate-significant challenge in retaining staff, up marginally (↑3%) on Autumn 2024.

National insurance contributions

This wave, we also asked organisations with paid staff to tell us what impact they expected the proposed increase in Employer National insurance contributions (ENICs) to have on their organisation. Seven in ten organisations (70%), thought the increased contributions would have a moderate-significant negative impact on their organisation’s finances and four in ten (41%) thought the same for their service or programme delivery. Only two percent (2%) thought it would have a positive impact on their finances and service or programme delivery.

There is however a significant difference in responses when we account for organisation size (turnover) and staff numbers. For large organisations (annual income £500,000+), 90% foresee a moderate-significant negative financial impact. For small organisations (annual income under £25,000) that number is half – 45% predicting a moderate-significant negative financial impact.

The same pattern is evident when you consider staff numbers. The more staff an organisation employs, the greater the negative financial impact is likely to be. For large organisations (employing more than 10 FTEs), 95% predict a moderate-significant negative impact, that number falls to 57% for smaller organisations – those employing between one and four members of staff.

Volunteer recruitment and retention

As with paid staff (Figure. 3), we asked organisations with volunteers to tell us if they had found recruitment or retention a challenge. Like paid staff, recruitment of volunteers has been more challenging than retention. Fifty-five percent (55%) of organisations reported a moderate-significant challenge when attempting to recruit volunteers. This is down (↓7%) from Autumn 2024. As for retention, almost 40% organisations found retention of volunteers to be a moderate-significant challenge in Spring 2025 – in line with Autumn.

We asked those organisations that reported challenges with recruitment and/or retention of volunteers to tell us what those challenges were. For seven in ten organisations (73%), the main challenge was fewer people coming forward to volunteer, followed by a belief that people have less time to volunteer (52%) and volunteer fatigue or burnout (41%). Figure 6. Illustrates the change in responses from Spring 2024-Spring 2025.

We asked those organisations that reported a challenge with recruitment and/or retention of volunteers to tell us what actions they’d taken to improve recruitment and/or retention. Over a quarter (27%) of organisations told us that they had looked to increase volunteer numbers by approaching people who don’t normally tend to volunteer for the organisation. A quarter of organisations had run a recruitment campaign, and a similar number had restructured roles to make them more flexible. One in five (22%) had sought advice from their local TSI, infrastructure organisation or other third sector organisation.

For the third (34%) of organisations that had taken no specific actions, we asked them to tell us what had prevented them from doing so. The most common responses included a lack of volunteer management support (35%); uncertainty over future service provision (24%) and being unsure where to start (15%). Thirty-five percent (35%) of respondents told us about something else preventing them from acting. Those responses included ‘too busy with service delivery’; ‘keep asking but nobody seems keen’; ‘not a priority right now’ and ‘we can cope with what we have.’

In exploring the overall financial health of organisations, we ask organisations about their turnover, financial reserves, cash flow, and confidence in their ability to continue operating.

Turnover

Half of respondents (52%) reported that their monthly turnover had stayed about the same over the past four months, in line with Autumn 2024. Approximately a fifth (22%) reported an increase in average monthly turnover and 24% reported a decrease. These numbers are broadly in line with Autumn 2024, with a small increase in the number of organisations reporting a decrease (↑3%) in their monthly turnover.

For the 24% of organisations reporting a decrease in monthly turnover, just under half (46%) believe this to be a medium-term issue, while a third think it will be more of a longer-term trend, lasting for more than a year – fewer organisations believe this decline to be a longer-term issue than in Autumn 2024 (↓11%).

Deficit budgets

A new financial question we included this wave was to ask respondents if their organisation was running a budget deficit, and if so, what impact that deficit has on their organisation. Six in ten (60%) said that they weren’t running a deficit budget, while 37% said that they were. Large organisations (turnover £500k+) were more likely to say they were running a budget deficit than smaller organisations.

There were 119 responses to the open question about the impact of running a budget deficit. The key themes to emerge included, organisations having to use their reserves; staffing reductions and salary constraints; cuts to services and activities; the negative impact on planning and increased uncertainty; increased efforts to generate income and an increased risk of closure or restructuring.

Many organisations report dipping into or relying heavily on financial reserves to cope with the deficit. While some organisations do have healthy levels of reserves, respondents are concerned about the long-term sustainability of continuing to use them.

“We will be required to use our reserves. We’ve had to make redundancies.”

“We are currently into our contingency funding to ensure services are remaining the same.”

“Eating into our reserves… our reserves policy requires us to carry 6 months of costs, but this is challenging.”

Some organisations have made redundancies, reduced staff hours, and report being unable to afford pay increases. There’s concern about retaining skilled staff and rising employment costs, including increases in national insurance contributions.

“We’ve already cut a number of core staff posts this year and will have to cut more in the near future.”

“The deficit budget and Employer NIC increase means we will be unable to afford a salary increase for staff.”

“We will need to look at cutting staff hours to accommodate and not be able to fully undertake the work.”

As the above organisation highlights, numerous organisations mention cutting back or scaling down services, ceasing non-essential activities, or halting planned projects and developments.

“We won’t be able to provide certain programmes and are looking at cost-cutting options.”

“We have had to reduce some of our services to the children and families that we support.”

“It will make it increasingly difficult… to maintain the levels of support currently provided.”

Several responses indicate active fundraising efforts, diversification of income, or increased reliance on trading activity. Some are asking people to contribute more or exploring new income sources.

Finally, some organisations state they may not survive beyond the next year without new income and that structural changes, downsizing, or even merging with other organisations are being considered.

“We will cease as an organisation and be taken over by other charities or organisations.”

“Continued deficit budgets over the next few years will force the leisure centre to close.”

“It is likely we will have to make structural changes to ensure sustainability.”

“If we cannot plug the gap it will lead to major restructuring or closure.”

Reserves

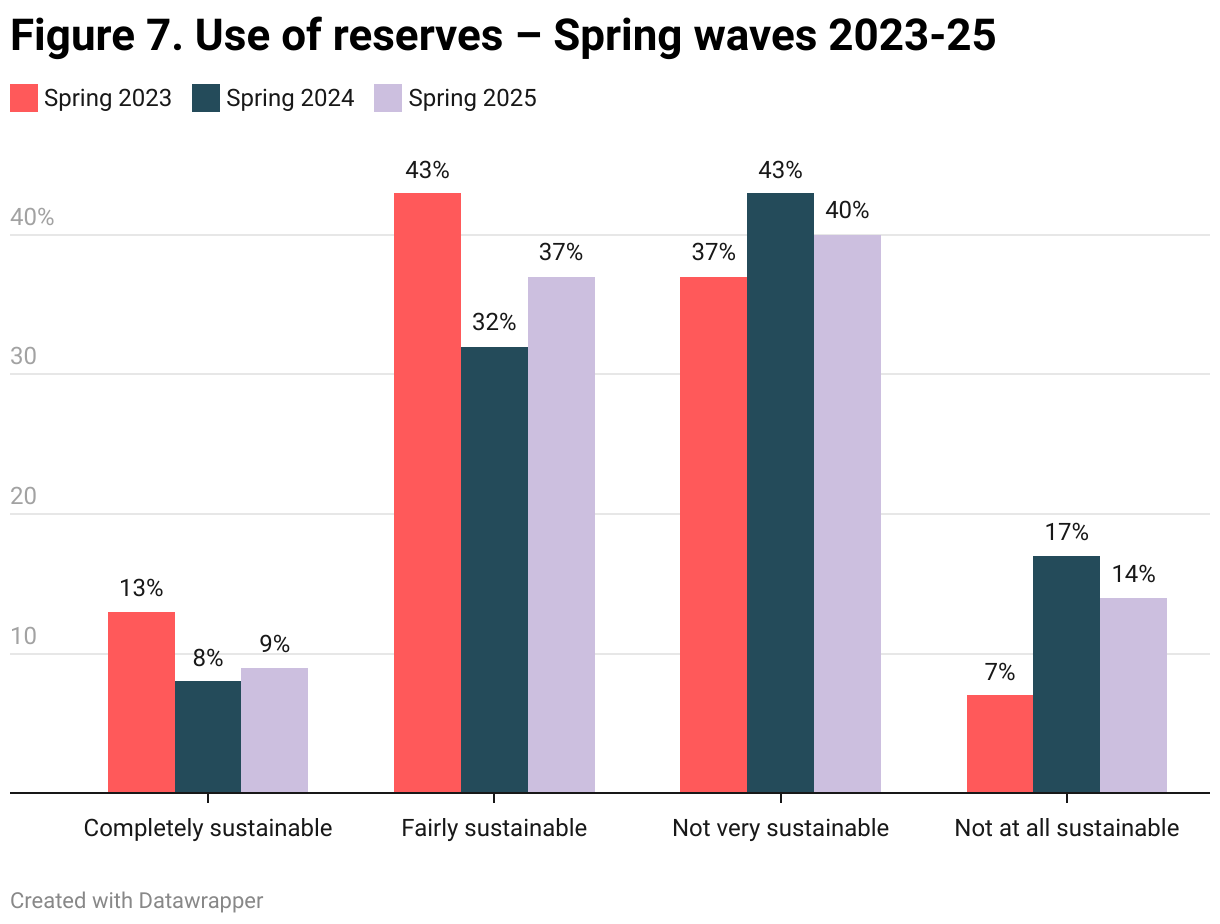

The percentage of organisations holding less than 6 months’ financial reserves remains stable at 53%. Similarly, the number of organisations that believe that their reserves are very important or essential to their short to medium term survival is 56% - a 5% increase since Autumn 2024. Unfortunately, the number of organisations reporting that the use of their reserves is unsustainable has risen to 54% - a sharp increase from 40% in Autumn 2024, but below the Spring 2024 peak of 60%.

Funding

For the first time this wave we asked respondents if they had their funding confirmed for the 2025-26 financial year. Just over one in three respondents (36%) hadn’t had their funding confirmed and almost half (45%) had some, but not all, of their funding confirmed. Only 13% of organisations has all their funding confirmed when surveyed in February-March 2025.

For those 13% (admittedly a small sample) of organisations that had all their funding confirmed, we asked them if the level of funding confirmed was as expected, less than expected or more than expected. Fifty-eight percent (58%) of organisations said the funding levels they had confirmed was as expected, 22% said more than expected and 13% said less than expected.

Organisations were then asked two questions on the topic of institutional funding sources. Respondents were asked if they had experienced any delays in funding over the past four months and if the conditions attached to their funding had become more demanding.

For organisations in receipt of institutional funding, 17% said that they had experienced delays in funding from Scottish Government (and decrease of 8%); 18% (↓4%) their local council and 21% (↑5%) reported delays in funding from another funding organisation. Just under half of respondents (46%) thought the conditions attached to their funding had become a little more or much more demanding in the past quarter – in line with Autumn 2024.

Outlook

Organisations were asked how confident they were that they will still be operating in 12 months’ time. Confidence remains high, with 89% of organisations confident that they will still be operating next Spring – in line with Autumn 2024.

For the second wave running, we asked organisations to tell us where they go for different types of advice and/or support and what advice and support they might need in the next 12 months. Forty-eight percent (48%) of organisations said that they had sought advice and/or support in the last 12 months – up 5% since Autumn 2024. The most common types of advice sought included, administration (38%); governance (35%); legal advice (30% ↓7%); advice on finance (29%) and IT and digital (29% ↓7%).

We then asked organisations to tell us where they had sought this advice and/or support. For administrative support, legal advice, IT and digital support and advice on finance organisations were most likely to approach a national membership organisation, such as SCVO. For governance support, organisations most often approached their local TSI.

Finally, we asked respondents to tell us what support their organisation would benefit from over the course of the next 12 months. The most common response was support to find funding (49%), followed by advice and support to help with recruiting volunteers (including trustees) (31% ↓4%) and IT and digital support (24% ↓5%).

The findings from the tenth wave of the Scottish third sector tracker highlight a sector that continues to face significant and evolving challenges. Financial pressures remain the most critical challenge, with increased costs, uncertainty, and funding shortfalls consistently cited as major concerns. A notable proportion of organisations are operating under budget deficits, increasingly reliant on reserves, and struggling to maintain service levels and staffing. While confidence in short-term survival remains relatively high, the sustainability of many organisations is clearly under threat.

Staff and volunteer recruitment, and to a lesser extent, retention, also persist as significant issues, and the anticipated impact of increased National Insurance contributions only adds to the financial strain. Despite these pressures, many organisations continue to deliver services successfully and are proactively seeking funding and other support to strengthen resilience.

This wave reasserts the importance of continued investment and support for the sector to ensure long-term sustainability and the ability to meet the growing needs of communities across Scotland.