The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

Our latest analysis shows more charities struggling to break even, but also some welcome growth in key funding streams

Our newly published analysis of 2022/23 financial data shows that while the sector’s overall income continues to grow modestly, sustainability remains a key issue.

Income from government has remained fairly steady, and income from the public has largely recovered after being hit hard by Covid. Unfortunately, for many organisations inflation and rising costs mean expenditure has outpaced any income increases.

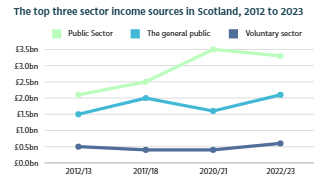

As we can see from the chart above, the public sector and the general public are the two most important sources of income for the Scottish voluntary sector. Five years ago, the amount of money received from government was just slightly higher than the income received from the public via donations and sales.

Covid saw that gap widen significantly. Money from the general public decreased in 2020/21, while we saw public sector funding boosted by £1bn.

There has now been a slight fall in the value and relative importance of public sector funding to the sector. Fears of a sudden withdrawal of essential government support were not realized in 2023, but when we factor in inflation these grants and contracts are now worth less to the sector, putting pressure on budgets.

Meanwhile in 2022/23 we saw income from individuals recover after a few hard years when Covid and the cost-of-living crisis seriously dented fundraising, sales and donations. Trading and fundraising income is now happily back on track, although straightforward donations are still subdued.

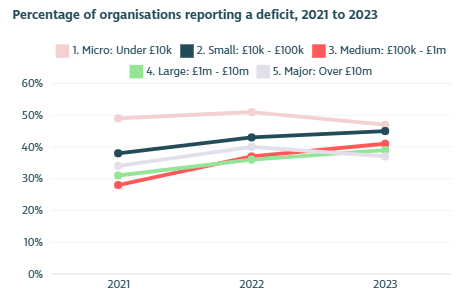

Inflation rose steeply over 2022 and 2023 and the sector has seen rising costs across many areas from staff costs to insurance and utilities costs. Many charities saw their heat and lighting bills treble and even quadruple in 2023. Despite the tough economic climate, over half of charities were still able to keep within budget in 2023. However, margins have tended to be wafer-thin. There has also been a steady rise in the number of small, medium and large organisations ending the year in deficit – see chart below.

Finding funding for activities and services is a perennial problem for the sector, and inflation and high costs are intensifying that pressure. Despite these challenges most (87%) organisations are confident of their survival showing the resilience and optimism characteristic of our sector. A similar proportion of organisations think they have the capacity to meet most or all current demand for services, albeit with an increasing number saying they have to expand their fundraising activities and adapt services to remain operational.

For our 10-page summary of the latest financial trends see State of the Sector 2024: key Scottish voluntary sector figures and trends.