The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

A resilient sector? The resilience of Scottish voluntary organisations 2025

The resilience of Scottish voluntary organisations

Introduction

This paper considers the available literature and data on the resilience of Scottish voluntary organisations. It looks at academic literature, primary and secondary data. For this paper, resilience is defined as the ability of an organisation to anticipate, cope with and adapt to disruptions while maintaining core functions. (Herrero, 2022). By examining the sector's response to events such as the Covid 19 pandemic and the cost-of-living crisis, alongside long-term trends from the Scottish third sector tracker, we draw conclusions about the sector’s resilience and what is required to sustain and build on that resilience.

The resilience of the Scottish voluntary sector depends on several factors, including funding stability, policy support, workforce capacity, and adaptability to external challenges like rising costs and policy changes. While the Scottish voluntary sector has demonstrated resilience in facing challenges (such as the pandemic and rising costs), ongoing financial insecurity and workforce pressures present risks. Greater investment in sustainable funding and workforce well-being will be key to maintaining and building resilience into the future.

- Financial insecurity remains a top concern, with 8 in 10 voluntary organisations citing it among their main challenges.

- Workforce pressures are significant, including recruitment difficulties, low pay competitiveness with the public sector, and concerns over staff wellbeing and burnout.

- The sector has demonstrated strong adaptive resilience, with most organisations maintaining or exceeding service delivery plans since mid-2022 despite external pressures.

- Service demand has increased steadily, with around 60% of organisations reporting rising demand quarter over quarter.

- COVID-19 had a major impact, prompting widespread service adaptations and shifts to remote and hybrid working models.

- Rising costs and inflation are a growing challenge, now ranked among the top three challenges by half of organisations (as of Spring 2025).

- Climate change is also a growing concern, with 41% expecting a moderate or severe impact and most identifying funding as the key barrier to building climate resilience.

- Digital technology is vital but understanding of and confidence in cyber resilience is uneven, with 31% of organisations feeling unprepared for cyber risks.

- Despite challenges, confidence in survival remains high, with approximately 90% of organisations believing they will still be operating in 12 months’ time.

- Future resilience depends heavily on financial health, with many organisations planning to adapt fundraising strategies, staffing levels, and service delivery to remain viable.

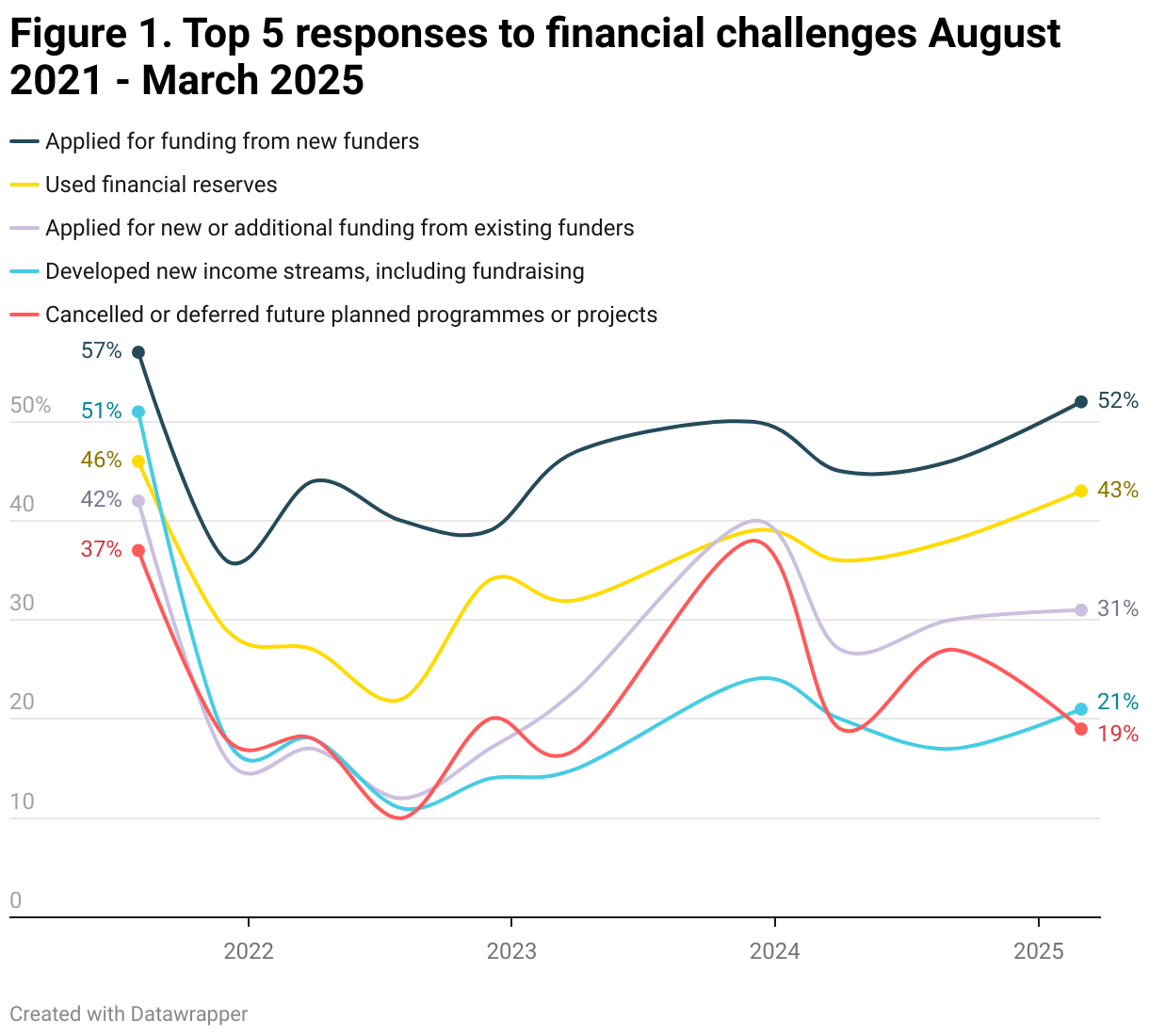

Financial risks, such as inconsistent funding and cash flow issues, are the most significant concerns for Scottish voluntary organisations (McDonnell, 2017). This is evident in the responses to the Scottish third sector tracker, where eight in ten organisations (as of Spring 2025) identify financial concerns in their top challenges.

Figure 1 illustrates that organisations have been proactive in adapting to financial challenges. The top five actions are highlighted below, ranging from applying for funding; using financial reserves; cancelling or deferring work and developing new income streams.

As Armstrong identifies in her paper on resilience behaviours in third sector leadership (2022), third sector leaders face unique pressures, including increased demand for their organisation’s services, reduced funding, heightened competition, and constant change—challenges that have intensified since the COVID-19 pandemic. The paper highlights the need to acknowledge and address the systemic causes of stress and burnout, including insecure funding and employment.

Many tracker respondents tell us that staff recruitment and retention is a challenge for their organisation and almost one in five (18%) report staff wellbeing as a concern. The key message from respondents is that the sector is not valued as a place to work and struggles to compete against the public sector, at least in terms of salaries. Organisations told us that they do not have the funds to retain or attract appropriately qualified staff and this is having a detrimental impact on service delivery and staff wellbeing and morale. There was also a feeling that the people applying for roles were not qualified. The issue seems particularly pronounced for rural based organisations and has only been exacerbated by Brexit.

Maintaining core functions

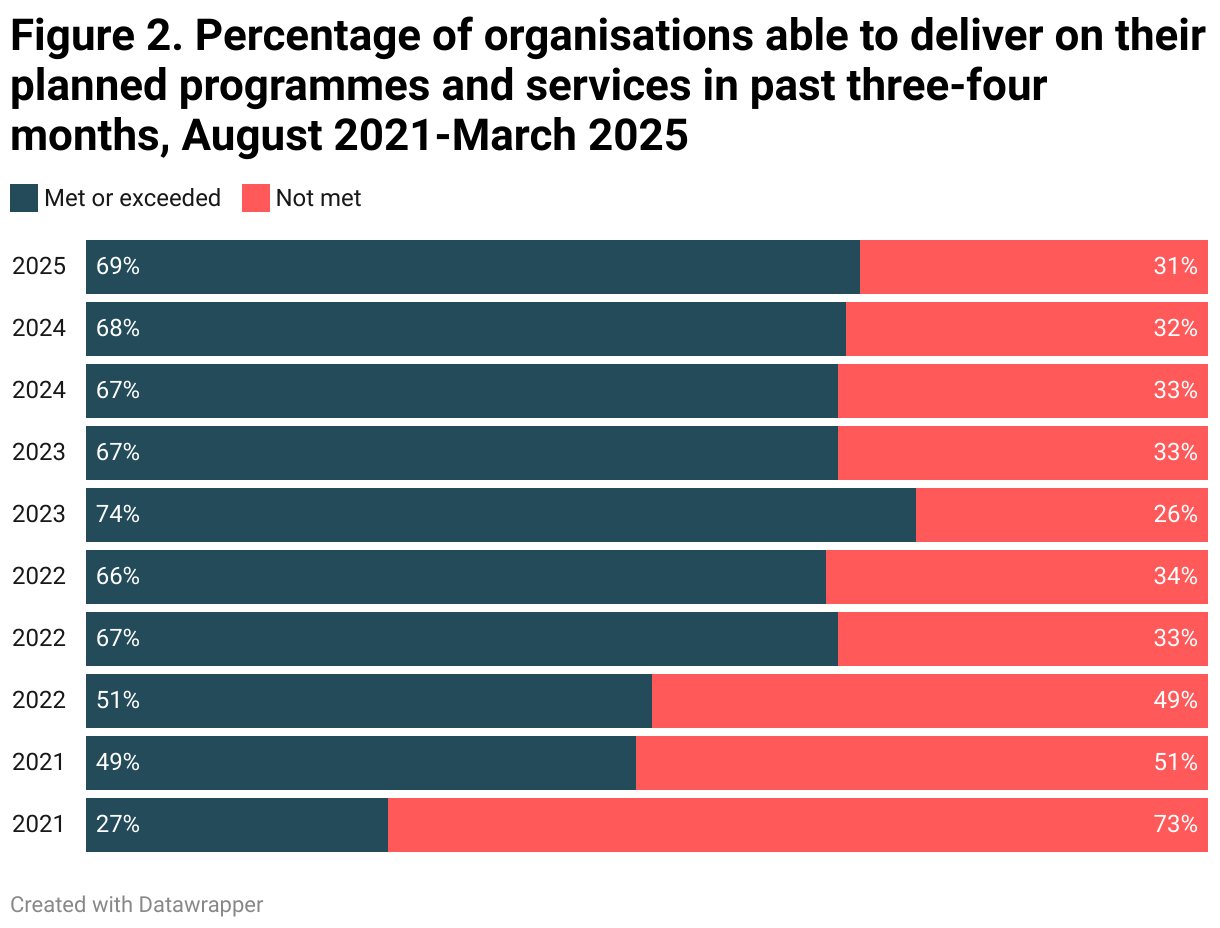

As per the definition, a hallmark of organisational resilience is the ability to continue to operate and deliver core services in the face of disruptions. Findings from the Scottish third sector tracker highlight the sector’s ability to continue to deliver. As figure 2 shows, organisations struggled to maintain services during the pandemic. However, since the summer of 2022, between two-thirds (66%) and three-quarters (74%) of organisations have met or exceeded their planned programmes of work over the preceding three-four months.

Meeting demand

Voluntary organisations have experienced a significant increase in demand for their services over the past few years, with panel data from the Scottish third sector tracker consistently showing about six in ten organisations reporting increased demand quarter over quarter.

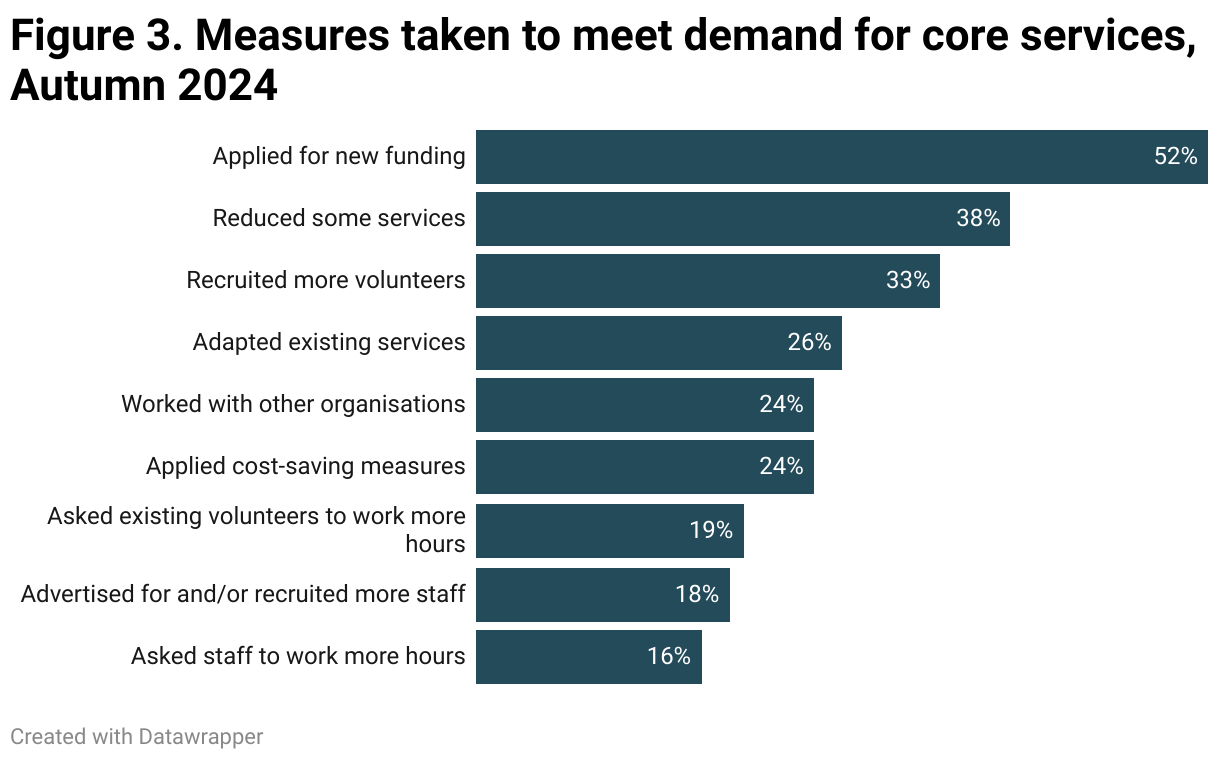

In Autumn 2024, we asked respondents to the Scottish third sector tracker what measures their organisation had put in place to address the challenges presented by increased demand for their core services. The most frequent responses included: applied of new funding (52%); reduced some services (38%); recruited more volunteers (33%); adapted existing services (26%) and worked in partnership with other organisations (24%).

Responding to the COVID-19 pandemic

Due to the changing nature of the COVID-19 pandemic, third sector organisations had to continually adapt their services to ensure they were complying with the most up to date guidelines whilst continuing to respond to the needs of their service users and beneficiaries. The majority implemented several adaptations allowing them to run their activities safely. Some had to suspend services that could not be adapted to remote delivery.

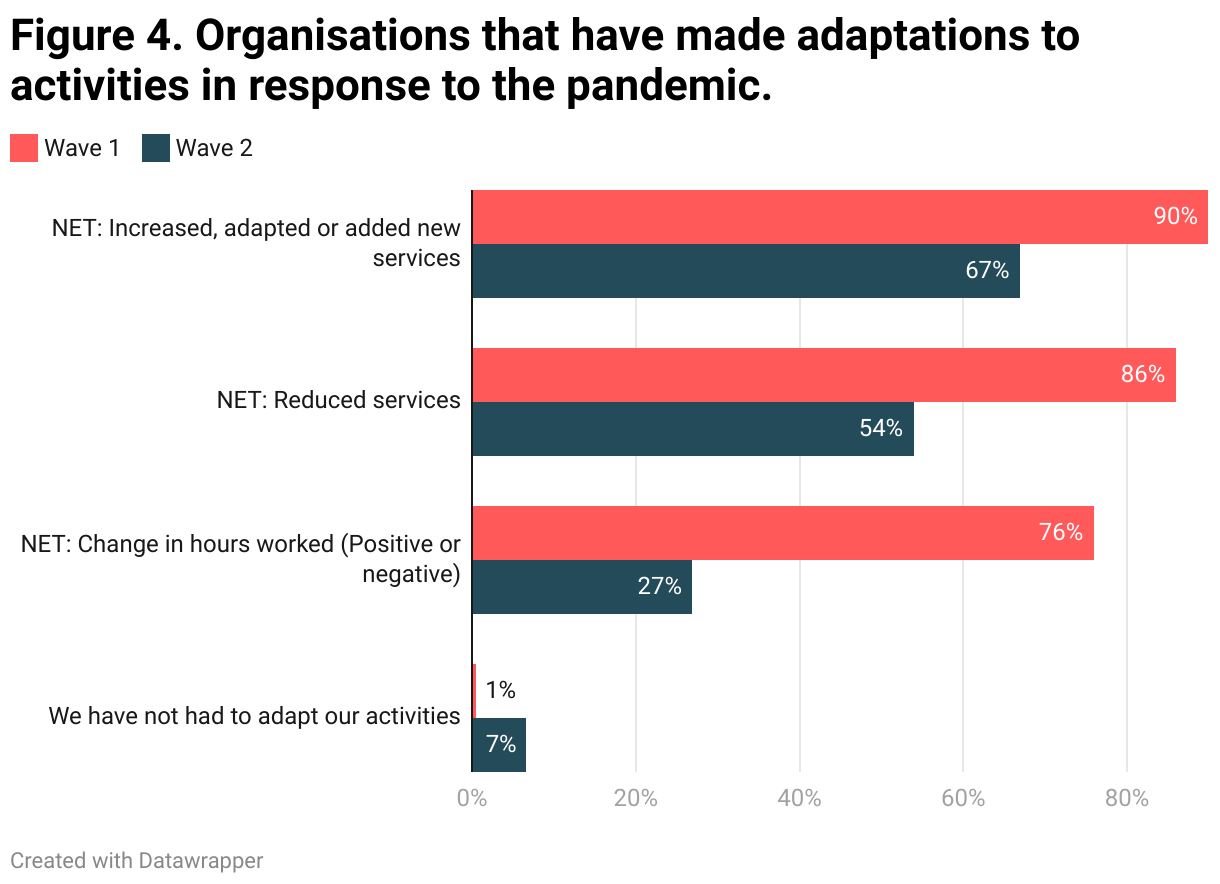

In August 2021 (wave one), organisations were asked which adaptions to activities they had made in response to the pandemic, and whether these were still in place come December that year (wave two). Most organisations in wave one (90%) indicated that they had increased, adapted, or added a new service. Adaptations to their normal ways of working included: adapting services to support different groups and communities (52%) or supporting people remotely by phone or online (79%). Organisations specialising in health or religious activities were particularly likely to say they had adapted services to support people remotely or online. In wave two, 67% of organisations indicated that they were still maintaining these adapted or new services.

Many organisations had to reduce their services during COVID-19, as indicated in wave one (86%). This was particularly high for organisations that specialised in religious activities (97%) and culture or sport (93%) as many of these organisations’ buildings were closed during the pandemic. By wave two, 54% of organisations were still operating with reduced services, increasing to 70% for those in culture and sport.

Over three quarters of organisations reported having changed staff working hours since March 2020 in wave one. Approximately 55% indicated that staff were working longer hours during this time and 27% said that staff were working fewer hours (excluding furloughing staff). By wave 2, far fewer organisations were reporting changed working hours (27%). Just 0.5 % of organisations said that they had not had to adapt their services or activities prior to August 2021.

The data emphasise how seriously the third sector was hit by the pandemic and the extent of the measures taken to ensure that needs were still being met despite the restrictions.

During the COVID-19 pandemic, many organisations had to move their services and activities online, and many staff and volunteers were working remotely. In wave 3 (Apr 2022), we asked organisations for the first time if they found managing the move to hybrid working difficult: 10% stated that it was one of the top 3 challenges they had faced in the past 3 months. In this wave, additional questions were asked about how organisations were running their services, programmes, or activities, whether mainly online or in-person. Detailed breakdowns and commentary on the following questions can be found in the wave 3 reports at the SCVO website.

In wave 3 (Apr 2022), organisations were asked to comment on the benefits and challenges of operating using hybrid methods of administration and delivery. The most frequently mentioned benefit of hybrid working was the positive impacts on service users (25% of respondents mentioned this), including their engagement, experience, and outcomes. For 18% of respondents, hybrid working has had a positive impact on their organisation’s resource levels, predominantly by reducing costs. As a result of adaptations, resource costs (including non-financial costs) have decreased, for example, time savings, lower travel, and premises costs.

The most frequently mentioned challenge of operating using hybrid methods was the negative impacts on staff and volunteers (29%), including culture and community building (14%), supporting, and managing staff remotely (7%) and the health and well-being of staff (7%).

Responding to rising costs

As well as responding to the uncertainty resulting from the COVID-19 pandemic, third sector organisations have faced new challenges with the emergence of the cost-of-living crisis during 2022 and 2023. This has been a multi-dimensional challenge for organisations, with direct impacts on operational costs, as well as impacting the people and communities that they work with.

Tracker results from wave 2 (Dec 2021) onwards show how organisations have become increasingly concerned with rising costs and inflation. In December 2021, rising costs and inflation were reported to be a top 3 challenge for 14% of organisations (see Figure 3.3). By wave 10 (Mar 2025), 50% of organisations chose rising costs and inflation as one of their top three challenges. Social enterprises are particularly concerned about this.

As organisations face more internal pressures from rising costs, many have had to adapt their services or activities to save money. Organisations were asked in waves 5 and 6 about the changes they have made to their operations in response to rising costs. At wave 6, 83% percent of organisations said they had made at least one change to limit the impacts of cost increases.

In both waves, the most frequent change that organisations made in reaction to rising costs was to seek additional funding, as indicated by nearly half the organisations (45% in wave 5, increasing to 52% in wave 6). Organisations that employed paid staff were more likely to have sought extra funding (60% of organisations in wave 6) than those without (34% of organisations). Whilst organisations that employ staff may have a larger cost base in general than those that do not, the findings may suggest that some organisations were seeking additional funding to enable them to improve staff wages, given that 30% reported to have increased staff pay and benefits to offset inflation in wave 6. The second most frequently implemented change in both waves was reducing or ceasing services, as many organisations considered how they could adapt their activities to save costs.

In Spring 2024 (wave 8) we asked organisations several questions relating to climate resilience. Forty-one percent of respondents expect climate change to have a moderate or severe impact on their organisation, whereas 54% expect a small or no impact.

Of those who believed climate change would have an impact, 80% believe it will be important for their organisation to be able to adapt to and/or build resilience to the potential impacts. Only 16% reported that this would be unimportant.

We also asked organisations to tell us what support they need to adapt and build resilience to the impacts of climate change. The key themes to emerge included funding; advice and guidance (including at a national policy level); and staff training.

Many respondents are knowledgeable about the climate crisis and are already taking steps to build resilience to its impacts. The major barrier is financial; funding is the most requested type of support. Capital investment is needed to upgrade and improve buildings; purchase electric vehicles and modernise equipment, for example.

In Autumn 2024 (wave 9), we asked organisations a series of questions about their use of digital technology and understanding of cyber resilience and risk. Firstly, we asked respondents to tell us how important digital technology is for the way their organisation operates and delivers services. For 85% of respondents, digital technology is either very important (47%) or quite important (38%). Only 4% think it not important at all.

We then asked respondents how well they understood cyber resilience and risk. Four in ten organisations (41%) believe they have a high level of understanding; a quarter have a low level of understanding, and the rest are somewhere in the middle. Following that, we asked respondents how confident they were that their organisation is well protected in relation to cyber risk. Sixty percent of respondents were confident and a third (31%) didn’t feel confident. Finally, we asked respondents to tell us what cyber security measures their organisation had in place. Reassuringly, only 5% of organisations said they had none of the listed measures. The most common measure to have in place was antivirus software (74%), followed by software updates and regular backups (both 61%).

As per the evidence in the above sections, organisations are being proactive and practical about the adaptations required to ensure their organisation can continue to operate. Additionally, when people are asked about the future direction (positive or negative) of their organisation, it’s clear that considerable thought has gone into the possible trends, changes and challenges to come.

In January 2024, we asked respondents to the Scottish third sector tracker two questions about their outlook for the next 12 months’: for their organisation and the third sector more broadly. As we might have expected, respondents are more positive about the outlook for their own organisation than the Scottish third sector more generally. Thirty-five percent (35%) of respondents thought that the Scottish third sector would be in a slightly worse position in a year, compared with only 20% of respondents who believed the same for their own organisation. There is also a 16% difference between those who believed that the sector would be in a much less positive position (22%) in a year, compared to only 6% who believed the same for their organisation.

We asked both those respondents that expected their organisation to be in a more positive position in 12 months’ time and those who expected their organisation to be in a less positive position, to tell us what trends, changes and challenges they expected their organisation to experience.

For those that said more positive, there were several key themes to emerge. The most frequently mentioned reason for respondents’ positive outlook was the belief that their organisation would be in a better financial position in 12 months’ time. This primarily included mentions of securing, or plans to secure, funding, either from existing or new funders, increased fundraising activities and further development of new and existing income streams.

On the other hand, many organisations were less optimistic about the future. For those respondents that thought the outlook for their organisation was less positive, the key theme was the same as for those with a more positive outlook – the financial health of their organisation. Many respondents thought that their organisation would be in poorer financial health in 12 months’ time. This included mentions of standstill, reduced or more competitive funding, the unsustainable use of reserves, challenges fundraising, and continued rising costs (including staff pay).

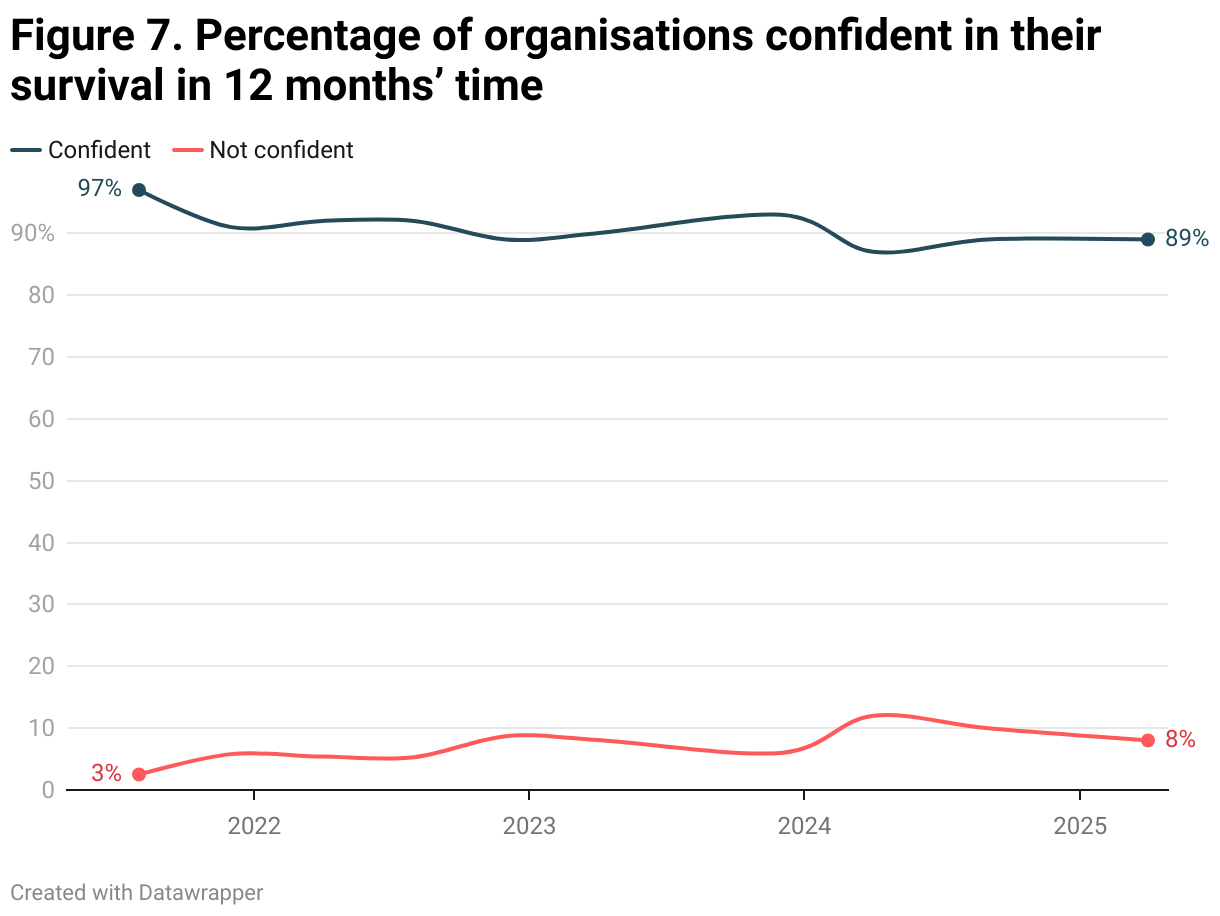

Having said that, organisations have remained confident in their future survival, with approximately nine in ten voluntary organisations confident they’ll still be operating in 12 months’ time. There has been a small increase (↑4%) in the number of organisations who are not confident in their survival.

In Spring 2024, we asked respondents to tell us what changes they expected their organisation to have to make to remain operational in 12 months’ time. The most common themes included funding and fundraising; staffing changes; reducing or adapting activities; and looking for new premises.

By far the most common response was funding and fundraising. Many respondents mentioned the need for increased fundraising, applying for new grants and trying to diversify their income sources. Specific mentions included, applying for more core funding, organising more fundraising events and looking for new funders.

The Scottish voluntary sector has shown remarkable resilience in the face of significant challenges, from the COVID-19 pandemic and rising costs to increasing demand and workforce pressures. Organisations have adapted by modifying service delivery, pursuing new funding streams, investing in digital and hybrid approaches, and prioritising staff and volunteer well-being. However, persistent financial insecurity and workforce challenges continue to pose threats to long-term resilience. Looking ahead, the sector's ability to thrive will depend on sustained investment, policy support, and targeted assistance to build climate and cyber resilience. While many organisations remain optimistic about their individual futures, concerns about sector-wide sustainability underscore the urgent need for strategic, systemic support. Building a resilient sector will require working in partnership, adequate resourcing, and recognition of the essential role the sector plays.