The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

Scottish Sector Stats: six highlights from 2021

The figures below are from SCVO’s Sector Stats 2022. As well as an overview of the latest key stats we’ve taken a more in-depth look into six highlights.

Most charity accounts analysed for the Sector Stats 2022 covered the period April 2020 to March 2021 and show the financial impact of the first year of the Covid-19 pandemic. Analysis of 2020-21 charity accounts gave us a snapshot of the financial health of the sector after the first year of Covid.

The figures confirm what organisations were telling us in the first waves of the Scottish Third Sector Tracker, and underline just how financially disruptive the pandemic was for the third sector in Scotland, but also reflect the resilience of the sector and how it adapted to meet increased demand and emerging needs.

Six highlights

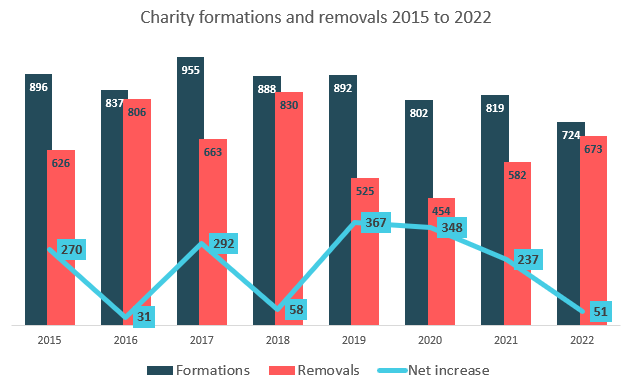

1. The number of charities being wound up dipped in 2020 but is now rising again.

Despite the pandemic, the number of organisations applying to OSCR for charitable status remained high, although with just over 800 new charities approved in 2020 and 2021 and 724 approved in 2022 the numbers are slightly down from 2019. We also saw a small drop in the net figures, with only 51 more charities being registered in 2022 than being wound up.

The number of charities winding up averaged 1.4 per day in 2020 and 2021, slightly lower than previous years and lower than might have been expected during the height of Covid. In 2022 the figure rose to 1.8 closures per day, but still below the average pre-2020 rates. Whether this is simply due to a lag in closures being reported to OSCR or annual fluctuation remains to be seen, and we need to wait at least another year to assess the longer-term impact.

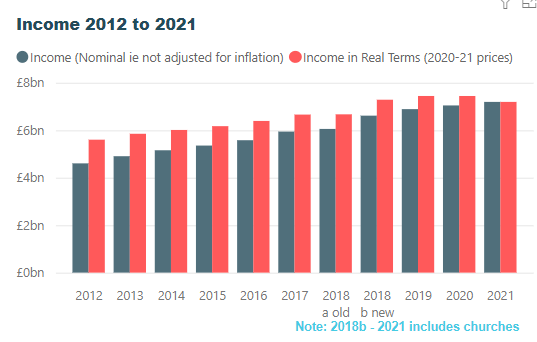

2. Sector income drops for first time in 20 years

In 2021 we saw the sector’s income drop for the first time in the two decades SCVO has been tracking Scottish charity finances. Scottish voluntary sector income rose by £149m (2%) to £7.2billion, but when we adjust for inflation that’s a real term drop of £250m (3%). While this drop can undoubtedly be attributed to Covid, it is important to note that income growth had already slowed in 2019, well before the pandemic hit, ending a long period of modest but steady growth.

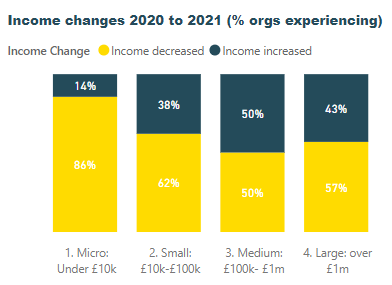

3. Small charities were hit the hardest financially in 2020-21

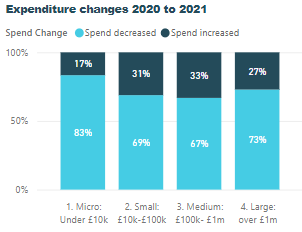

7 in 10 charities saw their incomes decrease during the Covid pandemic, but small charities (under £100k) were most likely to be negatively impacted. 8 in 10 small charities experienced a drop in income between 2020 and 2021, and 8 in 10 small charities also decreased their spending in this period.

On the other hand, almost half of medium and large charities' incomes increased, and over a quarter of them increased their spending in 2021. This highlights the very different experience Scottish voluntary organisations had in the first year of the Covid pandemic – one half of the sector had to close its doors, while the other half stepped up a gear to deliver existing and new services.

Looking at areas of activity, Housing, Social Care, and Community Development – where many of our larger charities are active - saw income increase, while Culture & Sport – where organisations tend to be smaller - saw a decrease. Income and spending also fell in the Health sector, reflecting that most of the sector is involved in secondary not primary health care, with many health-related activities paused due to lockdowns and social distancing.

It's important to note that this does not reflect money simply being shifted from small charities to larger charities, but reflects that much of the crisis funding and additional grants went to larger charities due to the types of activity they carry out, and to those with staff due to things like the furlough scheme.

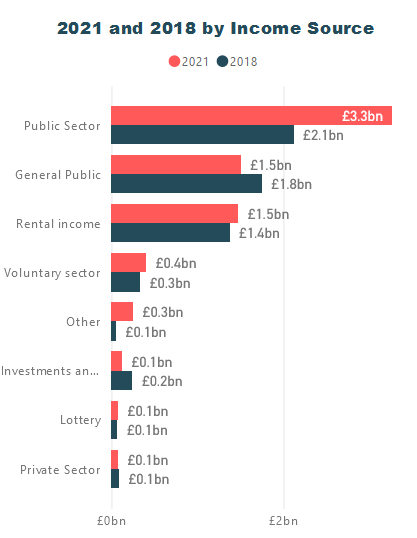

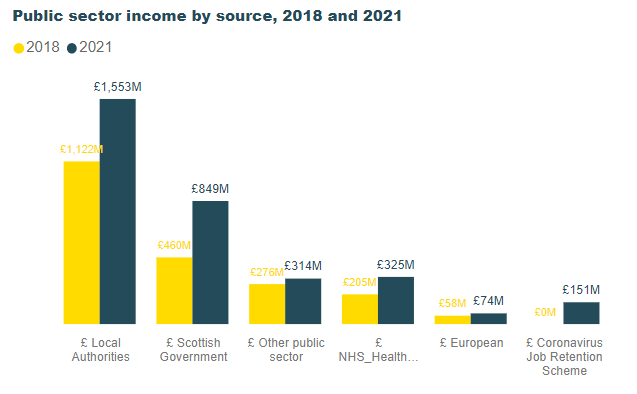

4. An additional £1bn of public sector funding came into the sector in 2021

Public sector income rose from £2.1bn in 2018 (£2.3bn when adjusted for inflation) to £3.3bn in 2021. Public sector funding usually makes up around a third of the sector’s income but jumped up to 46% of sector income in 2021 due primarily to Covid and the additional funds that were made available. Grant income from the public sector increased by two-thirds, from £0.9bn in 2018 to £1.5bn in 2021.

Scottish Government grants saw large increases, alongside the Job Retention Scheme and grant funding from the UK Government and bodies such as Creative Scotland. Much of this funding was in the form of emergency grants to organisations and it is likely we will soon see public sector grants drop back closer to pre-Covid levels.

Contract income also rose in value to £1.8bn in 2021, after a period from 2012-2018 where the real term value of contracts sat steadily at around £1.4bn. The value of Local Authority contracts rose from £1.1bn to £1.5bn between 2018 and 2021, while NHS and Health and Social Care Partnership contracts increased from around £150m to £270m. The increase in contracts primarily reflects the additional funds made available to support social care organisations and their staff. To what extent these increases are temporary or longer term remains to be seen.

Note: Figures here mainly compare 2021 data with 2018 data, when we last carried out detailed analysis of charity accounts.

2021 also saw a small shift from earned income to voluntary income sources

In 2021 63% of sector income came from earned sources such as contracts, fees and trading, down slightly from 67% in 2018. The key driver behind the shift was a sharp rise in voluntary income (i.e. donations and grants) from £2.2bn to £2.6bn. As highlighted above, there was a huge increase in public sector grants, and independent funders also stepped up their grant-making with an additional £100m.

In cash terms, earned income actually increased slightly, from £4.48bn in 2018 to £4.55bn in 2021, mainly due to the increase in contract income. However, earned income from the public fell due to the drop in in-person trading activities, as theatres, charity shops and cafes had to close their doors. Donations and fundraising income were better at weathering the pandemic, due to the huge effort charities put into their online fundraising. We even saw some large cryptocurrency donations making an appearance in 2021.

While much of the sector’s in-person trading income dropped sharply, some activities for generating funds such as hospice lotteries continued to do well during the pandemic, and the twenty Postcode Lottery charities go from strength to strength with a combined turnover now of over £500m. We also saw trading income recover in 2020/21 for some charities that were able to open to socially distancing visitors, e.g. zoos and gardens.

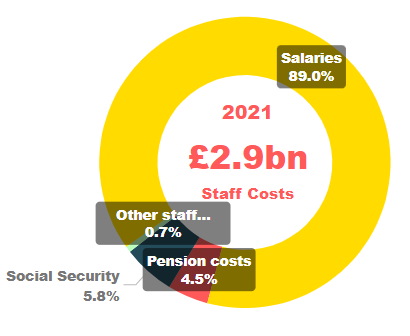

5. Staff Costs make up 43% of sector expenditure

The sector now employs around 135,000 people, with half employed by health and social care organisations. While only 3 in 10 charities employ paid staff, wages make up a significant part of the sector’s expenditure. Staff costs rose by £0.5bn between 2018 and 2021, from £2.4bn to £2.9bn.

While around half of the rise can be attributed to a small increase in the number of staff, we also see the impact of rising wages.

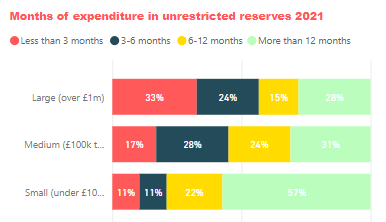

6. 1 in 10 charities have less than 3 months expenditure in reserves

Sector assets overall appear to be in surprisingly good shape, given that in the first wave of the Scottish Third Sector Tracker 46% of organisations reported using their reserves to help meet the financial challenges they faced after March 2020. The sector’s healthy balance sheet seems to be due to a couple of factors, primarily the rise in value of property and investments.

However, a quarter of charities had less than 6 months expenditure in reserves in 2021, and 1 in 10 had less than 3 months. What is interesting here is that it’s large charities who seem to be in poorer financial shape, with 1 in 3 large charities having less than 3 months in reserves. This is partly due to the figures being a ratio of expenditure to reserves – and large charities have large expenditures, while many smaller charities saw expenditure drop during Covid.

Note that the accounting period these stats cover ends before the huge rises in energy costs and inflation rates hit, which will inevitably have an impact on organisations and their financial resilience. We will be looking at the impact of this in our analysis of 2021/22 and 2022/23 financial data.

For more Sector Stats including interactive maps, charts and tables go to https://scvo.scot/research/facts-figures.