The Scottish Council for Voluntary Organisations is the membership organisation for Scotland's charities, voluntary organisations and social enterprises. Charity registered in Scotland SC003558. Registered office Caledonian Exchange, 19A Canning Street, Edinburgh EH3 8EG.

Public Sector Funding 2025

Public sector income - key sources and trends

Updated Public Sector Funding figures for the latest financial year (2024/25) are due to be published early Autumn 2026.

Public sector funding of the voluntary sector

The following pages pull together what we know about public sector funding from the latest SCVO Sector Stats, based on analysis of over 600 charity accounts, with additional information from the Scottish Third Sector Tracker and other sources.

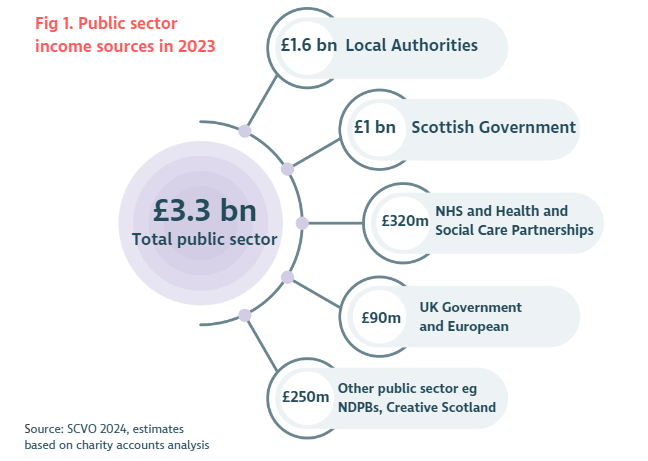

The public sector is currently the single most important source of income for the Scottish voluntary sector, worth around £3.3 billion in 2023. There has been a slight fall in the value and relative importance of public sector funding to the sector now that Covid-related funds have ended, combined with the impact of inflation.

- Public sector funding made up 40% of the sector’s income in 2023.

- Funding from the public sector was worth an estimated £3.3bn in 2023.

- Funding has stayed at 2021 levels in cash terms but fell by 5% in real terms (-£177m).

- Only 4 in 10 voluntary organisations get public sector funding, but for many it is critical.

The public sector is the single most important source of income for the Scottish voluntary sector. The sector’s growth over the last two decades has been driven by increased activities around public service delivery and recognition by policy makers that community-run services and facilities have the potential to offer better quality, better value and more sensitivity than large-scale ‘top-down’ statutory provision. Over the last decade around 40% of the sector’s total income has come from Local Authorities, Scottish Government and other public sector funders.

Public sector funding can be vulnerable to large fluctuations, such as the cuts seen following austerity measures and large-scale public sector funding cuts seen between 2010 and 2013. In recent years we saw government funding jump by £1 billion in response to Covid, emergency grants, Furlough and recovery funding - see fig 2.

Five years ago, government funding was only slightly higher than income received from the public via donations and sales. Covid saw that gap widen significantly as income from the public fell and public sector funding was boosted to almost £3.5bn. There has been a slight fall in the value and relative importance of government funding in 2023 now that emergency Covid grants, Furlough money and business recovery funds have ended.

Fears of a sudden substantial withdrawal of government financial support have not been realised, but while public sector funding has stayed at 2021 levels in cash terms, its real term value has fallen by £177m (5%), resulting in stand-still or tightened budgets for many.

Public sector funding made up 46% of all sector funding in 2021, but fell back down to 40% of total sector funding in 2023.

Local Authorities are the main public sector funder of the voluntary sector and account for half of all public sector money (£1.6bn in 2023), a proportion that has been fairly constant for over a decade. There has been however been a slight decline in the real-term value of local authority funding since 2021.

The Scottish Government is the second most important public sector funder. We have seen funding from Scottish Government increase in recent years, in large part due to Covid and post-Covid recovery grants but also other funding such as Mental Health, Equalities, Children & Families and Land funds (see fig 4 below).

NHS and Health and Social Care Partnership funding has slowly but steadily increased to £340m, reflecting a shift from mainstream Local Authority funding.

The £250m received from non-departmental public bodies (NDPBs) is also critical, and many NDPBs supported organisations with additional funds during Covid. These funders are particularly important for some sub-sectors e.g. culture (Creative Scotland), heritage (Historic Environment Scotland), and sport (sportscotland).

We also saw a slight increase in UK funding during Covid, mainly due to the Furlough Scheme. This has now dropped back down again, but is still significant due to Levelling Up monies (including UK Shared Prosperity Fund).

We have seen public sector income increase over the last two decades, with a shift away from grants towards contracts and more procurement-based models - see figure 5 below.

- Covid saw a reversal of this trend towards more contractual funding, with a large jump in grants due to the large number of emergency and recovery grants made available.

- Grants were worth £1,470m in 2023, a small £8m increase on 2021. However, grants saw a £78m drop in real terms from 2021 when we take into account inflation.

- Contracts made up £1,810m of the voluntary sector’s income in 2023. In cash terms this was a small £5m increase on 2021, but the real term value of contracts fell by £100m. This drop is perhaps more unexpected and more concerning than the fall in grants, as contracts tend to be related to ongoing service delivery.

For more on contracts and procurement see: The voluntary sector and Procurement – a summary of current voluntary sector experiences.

Macmillan, 2010"There is a lively ongoing debate within the sector about the pros and cons of different types of funding arrangements. This covers, for example, the purported shift from grants to contracts, and the extent to which this might add to or detract from third sector organisational autonomy and sustainability. The strength and vitality of the third sector will become increasingly salient in an emerging era of constrained public finance” (link)

- 4 in 10 voluntary organisations receive some form of public sector funding.

- Larger organisations are more likely to be in receipt of government funding, and more likely to be funded via contracts.

- Around 60% of medium and large organisations receive funding from local authorities, and around half receive funding from the Scottish Government and other public bodies.

- Almost 3 in 10 small charities receive some funding from local authorities.

- Most charities rely on a mix of funding streams, but a minority receive over 90% of their funding from government with many of these relying heavily on one or two key funders.

The picture for public sector funding in Scotland is slightly different from the wider UK one.

If we compare the green line in the two charts below, we can see that the public sector is the top income source for the Scottish third sector, but second for voluntary organisations across the wider UK, due to the presence of more large UK-wide donation-funded charities and also the slightly smaller role the voluntary sector plays in public service delivery in the wider UK.

The biggest difference however is that over the last 10 years the Scottish voluntary sector has seen public sector income increase slowly but steadily, with an extra boost during the peak of the pandemic and only a shallow decline as we entered the 2022/23 recovery period.

Meanwhile in the UK we can see that public sector income has been slowly decreasing in real terms over the last decade, and while we saw a similar boost during Covid, the UK then saw public sector income fall sharply from £17bn to £14bn in 2021/22 (2022/23 data not available yet) – see NCVO’s UK Almanac for more.

There is very little official data available on how much public sector money goes to voluntary sector organisations, so we currently use estimates based on detailed analysis of Scottish charity accounts.

Very few public bodies track whether their funding recipient is a voluntary organisation or social enterprise, despite government commitments to things like improving the third sector’s experience of procurement and increasing the number of social enterprises in Scotland.

There are currently calls for a ‘Civil Society satellite account’ to make the voluntary sector more visible in the National Accounts, as well as a call for public sector funders to make their funding more transparent on their own websites or via sites such as 360 Giving.

The Scottish Government has started to link data from the Scottish Procurement Info Hub with the Social Enterprise Census and estimates that Scottish public body procurement spend in Scotland with charities and social enterprises was approximately £944 million in 2021. However, this is recognised to be an underestimate as it does not include all organisations or money coming via non-procurement routes.

Given this gap, the data used in this report is therefore based on SCVO’s bi-annual analysis of around 600 to 800 charity accounts, weighted to be representative of the sector - see our Sector Stats Methodology paper for details. While overall figures are robust there may be some minor issues relating to attribution. For example, a charity may say in their accounts that they received money from their local council, but that money may have originally come from the Scottish Government or the UK Shared Prosperity Fund.

Delivering public services has long been a key part of the sector’s role and can offer greater stability for organisations and better quality services for service users. While many in the sector have welcomed the move towards more formal funding relationships with government, there are associated tensions and questions for the sector to try to balance.

Macmillan’s Third sector delivering public services evidence review highlights six themes:

- compromised independence

- ‘mission drift’

- loss of responsiveness and innovation

- employment conditions

- inter-organisational relationships

- polarisation within the third sector

Realistically we are unlikely to see public sector funding of the third sector rise substantially. Based on the trends we’ve seen and the current economic environment it is likely that many organisations will see below inflation increases, if not stand-still budgets or outright cuts.

In the most recent wave of the Third Sector Tracker 16% of respondents thought that their local authority was planning to decrease or withdraw their funding and 8% thought the Scottish Government would be decreasing funding.

Local authorities have had a real terms increase to their 2025/26 budgets, but given the pressures on their budgets it is unlikely that the sector will see much of that additional funding, although it may help mitigate some pressure points, eg increased Employer’s National Insurance Contribution costs.

We have also seen cuts to some important specialist income streams such as Creative Scotland funding as well as cuts to things like International Aid, which will have implications for many organisations, especially those which rely heavily on a single main funder.

Recent announcements of cuts to things like welfare budgets are also likely to have an indirect knock-on effect by increasing demand for some services.

If ‘more money’ isn’t a realistic option, how can the public sector and third sector work together to make the most of tight budgets and deliver the outcomes and services we both want to see?

Fair Funding is central to a sustainable voluntary sector in Scotland. It includes:

- multi-year funding

- sustainable funding, including inflationary uplifts

- flexible funding

- accessible funding, including timely notifications

Longer-term, multi-year funding

The sector has been calling for longer-term funding for over a decade, and while the government has been supportive in principle, progress has been slow. Recently Scottish Government and Creative Scotland have run pilots of two-year and multi-year funding. This is still the exception, and is only available to a small fraction of organisations, but is a welcome step.

Accessible funding

Delays in funding can cause disruption and stress. A quarter (25%) of Tracker respondents in Autumn 2024 said that they had experienced delays in funding from Scottish Government (an increase of 6%); 22% had experienced delays in funding from their local council.

Not all improvements require additional funding, but can be about making processes more efficient and flexible. The government have committed to timely notifications which will hopefully reduce these delays and uncertainty.

Last year the Economy and Fair Work Committee published the findings of its enquiry into the Procurement Reform (Scotland) Act 2014. The Committee found that while the Act has had a positive impact on increasing the transparency of procurement processes, “inconsistency, bureaucracy, and inflexibility are still creating challenges for small businesses and third sector organisations.”

As part of SCVO’s own submission to the Committee we looked at a range of reports about the experiences of voluntary sector organisations wanting to engage in public sector contracts and the procurement process, and found that there was a broad consensus:

- Good policies are in place, but there is still a disconnect between policy and practice on the ground.

- More still needs to be done to encourage and facilitate participation of third sector organisations in procurement.

- Significant barriers to third sector organisations’ participation in procurement work remain – the most frequently cited barriers are the complexity of procurement processes, short term contracts, poor terms and conditions, and a lack of engagement with contracting authorities despite the legislative aims.

There does appear to be a shift towards more flexible and collaborative models, and increased efforts to engage more voluntary organisations and social enterprises.

For more on voluntary sector funding and current funding issues see:

The voluntary sector in numbers – key facts

There are over

46,500

voluntary sector organisations in Scotland

In a typical year,

4 in 5

households use a voluntary sector service

Almost

1 in 3

people said they had used a services by a charity in the last 12 months (OSCR 2022)

43%

of young people said they had used a service provided by a charity in the last 12 months (OSCR 2022)

In 2024 the voluntary sector’s turnover in

Scotland was

£10.6bn

In 2024 the voluntary

sector spent

£10.4bn

on carrying out its activities

In Scotland last year

over 1 million

people volunteered

The sector looks after substantial assets on behalf of the communities and people of Scotland… from historic buildings, social housing and community land to investments held by charitable foundations, totalling an estimated

£37bn

last year

There are over

200,000

trustees leading charities across the country

Scotland’s voluntary

sector has

136,000

paid staff

88%

of voluntary organisations in Scotland are local

The voluntary sector

plays a particularly

important role in rural

communities – with

34%

of organisations based in rural or remote areas

The sector is made up of, among other things:

- 23,800 registered charities including 163 housing associations

- Around 1,000 community interest companies

- 83 credit unions

- Over 6,000 of these voluntary organisations are also social enterprises

Learn more about the sector’s size and shape and get in touch with our research team if you'd like to know more.